It’s been two months since my last update on my covered call strategy on $F while I wait for a dividend to be reinstated. As outlined in my first post, the ~6% dividend Ford was offering in 2019 was the primary reason I started accumulating shares. With the COVID “crash” in March the dividends were “suspended” while the company stabilized. That was probably the correct move for the company’s longterm future, but that doesn’t mean I didn’t miss those quarterly payments!

With that in mind, I started selling covered calls at strike prices above my average price to generate some income on that tied up capital I had in Ford. As the share price has rebounded, I have found myself in the money on my positions, but I have still been able to roll them out for an acceptable rate of return.

As of my last update, I had two February 19 covered calls, one at $9 strike and $10 strike. I had taken in $67 in credits before commissions. $F is now trading in the mid-$11s. Since then, I have been able to roll both of those out to March for another credit.

On January 22, I rolled the $9 covered call out to March 19 for a net credit of $16.68. This is a 1.9% return over 57 days, which is 11.9% annualized. With that credit, I bought one additional share for $11.47. This is similar to a DRIP (Dividend Reinvestment Program) with a traditional dividend.

On February 2, I was able to roll the $10 covered call out to March 19 expiration for a net credit of $31.68. This is a 3.2% return of 46 days, which is 25.1% annualized! As of now, I haven’t reinvested that credit and have just kept the cash.

This brings the total net credits from selling covered calls to over $115. At a current share price of $11.58, that’s a return of 5% over the course of about 3 months.

These positions, especially the $9 strike, are sitting pretty far in the money at this point. This means that there is very little extrinsic value remaining in these contracts, which means sooner or later I will choose to let it expire at have the shares called away. Fortunately, I have more than 200 shares of $F that I’ve own for more than 1 year, so my gains on those shares will be taxed at longterm capital gains if I’m forced to sell when they’re called away (to be clear: all the credits I’m receiving for selling the covered calls are taxed as ordinary income, unfortunately). If the stock price sees a pullback down below $11 again, I will look at rolling these out again as it’s likely there will be some more extrinsic value again. As long as I can get a 1% net credit for rolling out between 1 to 2 months, I think it will still be worthwhile as that’s a 6-12% annual return that, I feel, is pretty low risk.

I do expect Ford to resume the dividend at some point, so it would be nice if I could continue to roll out until then. But if Ford continues to climb higher and I get further and further in the money, that becomes increasingly unlikely. Either way, I will continue to update the blog with what happens.

Disclaimer: I am long $F. I am not a financial advisor. This is not investment advice. Please do your own research before investing in anything discussed herein.

First off, HAPPY NEW YEAR! This is not a yearly recap post and since I just started this blog a couple months ago, I’m not sure I will be making one. I will likely have a forward looking 2021 post though. Now, onto the post…

After two months of this experiment, I had put a total of $187 towards my mortgage principal from options trading profits which will equal $288 of interest saved over the course of my 30-year 3.125% loan. In addition, my options trading account principal of $3,200 (which was/is funded from savings from refinancing) was up to $3,240.86. A great start and already ahead of my initial goal by 2.6%.

I have continued to outperform in December, my third month, with $170 in options trading profits which is a 5.1% return on capital! In addition, my principal has grown to $3,498.35, 6% more than the $3,300 added to the account thus far. Remember, that 6% is after deducting taxes and withdrawals from the account to make the extra mortgage principal payments.

This month I have made a dramatic tweak to how I am divvying up my options trading profits towards my extra mortgage principal payments. More on that after I review this month’s positions and trades.

My positions & trades

$AAL, 100 shares at $13.98 average ($1,398 total principal). Principal is currently up 15.4% ($215.08), however I currently have a $15.50 covered call position expiring on January 29, limiting my capital gains to $152 total. I closed two positions for the month and for a profit of $74. I collected a net credit of $12 after rolling up from a $15 strike position to the current $15.50 position.

Going forward I will most likely continue to sell the $15.50 strike even if it stays in the money. I should be able to collect a large credit at least one more time. I will consider moving up to the $16 strike if I can still collect a decent credit. My main objective here with this account is to generate income, with a secondary goal of capital preservation and tertiary is capital growth, however I don’t want to leave easy money on the table in the name of current income. Like so many things in life, it is a balance.

$FCEL, no open positions. This month I finally had my shares of FuelCell Energy called away. In the end, I made about 30% in profits from that position. BUT I missed out on a $1,000 profit! This was a classic case of picking up pennies in front of a steamroller. In my defense, the pennies were very shiny and no one could have seen that steamroller coming!

I only closed that final $2.50 covered call for a $10 profit. On to the next one!

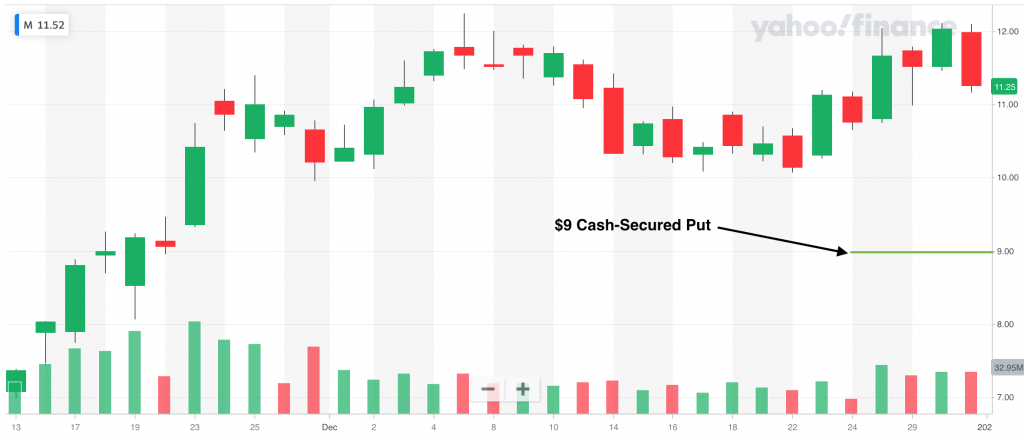

$M, no open stock position. Last month I had my Macy’s position called away at $6.50. I had just about given up on the stock when I saw an easy trade by selling a $9 Put for January 15 for a credit of $15. This trade is a 1.7% return (26% annualized), so it meets my 1% goal.

If the stock drops suddenly to below $9 and I am assigned, I expect the premiums to go up and good potential for selling covered calls.

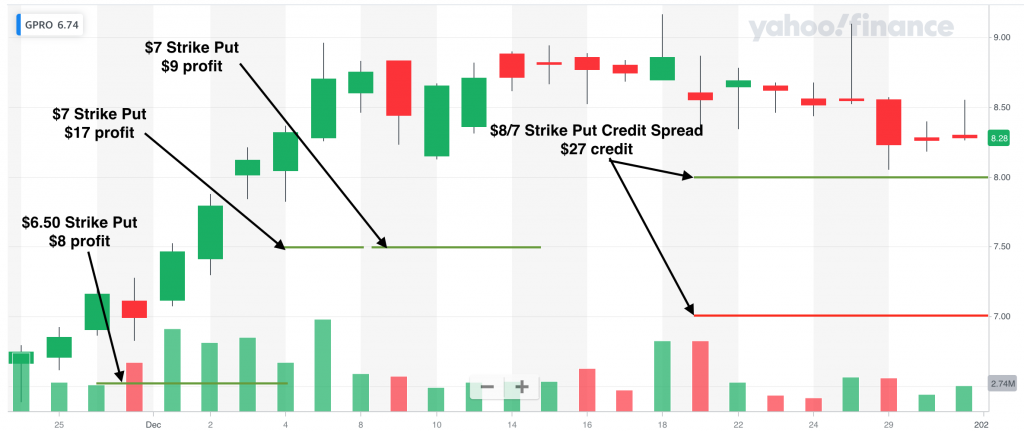

$GPRO, no open stock position. Similar to Macy’s, Go Pro was a stock that was called away from me in November. I decided to sell some puts this month, and that worked out well for me. I closed three positions for $34 profit. My highest strike price on those positions was $7.50, so that $34 was made using $750 as collateral, which is a 4.5% return.

I currently have a put credit spread at the $8/$7 strikes that I collected a credit of $27. In the past couple months I have had a lot more success with simply selling naked positions (cash-secured puts or covered calls, technically) than with credit spreads. However, more recently I’ve found some decent success with credit spreads as long as I’m willing to roll it out when I’m challenged. Contrary to a lot of advice, I am generally able to do this while collecting a credit if I widen the spread. So if I start with a $1 spread, I roll it out and down (for a Put) or up (for a Call). I’m therefore increasing my potential loss, which is why it generally isn’t advised, but it’s working for me right now so I’m going to go with it.

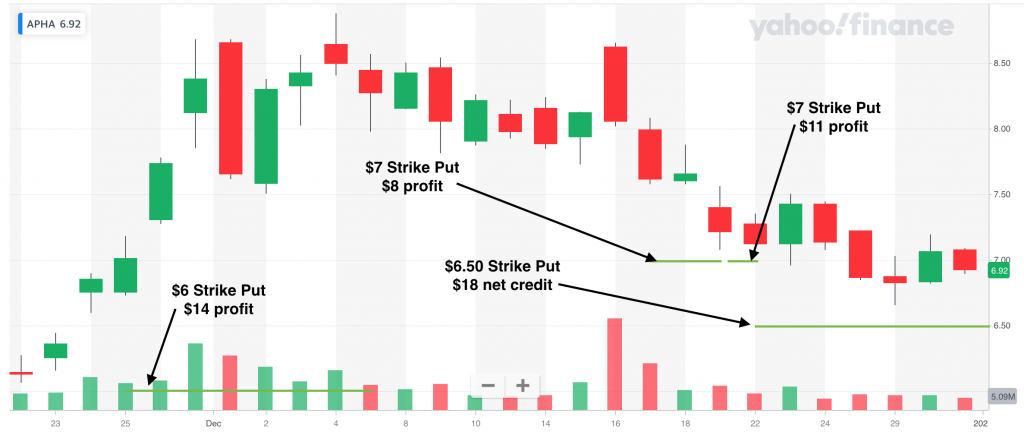

$APHA, no open stock position. I continued selling cash-secured puts on Aphria this month for some decent profits. I’ve thus far avoided getting assigned the stock. I closed three positions for a total profit of $33. Similar to the $GPRO puts, those $33 were earned with a maximum collateral used of $700, so a 4.7% return.

I currently have a $6.50 cash-secured put for January 15 open that I am watching closely. I collected a net credit of $18 after rolling down and out from December 31 $7 strike. That’s looking like a pretty smart move since it closed at $6.92 on New Year’s Eve and I would have been assigned. I may look to roll down and out to the $6 strike if I am able to for at least a 1% credit (i.e. $6).

$MRO, no open position. I had one trade on Marathon Oil Corporation this month, a credit spread from $5.50 to $4.50, with a profit of $9.

$MAC, no open stock position. I have an open credit spread on The Macerich Company (a REIT) from $9 to $7.50. I collected a credit of $13.

Extra Mortgage Principal Paid

As I said earlier in the post, I’ve changed how much of my profits I am putting straight into my mortgage principal. Perhaps this deserves its own lengthy post, but essentially I am wrestling with the opportunity cost of locking those profits up into the equity in my home. Now don’t read this as my giving up three months in.

As I listen to more finance podcasts and Youtube videos, I often hear about the velocity of money. When money is moving, it has velocity. Option trading is great because you are constantly moving money from one opportunity to the next. The money has velocity. When a dollar goes into my mortgage principal, it comes to a screeching 3.125%-halt. Remember my goal, which I am currently outperforming considerably, is 1% a month or 12% a year! Wouldn’t it be great if I could keep the velocity going before slowing it way down with my mortgage?

Of course it would be. However, the only reason anyone ever put extra principal into a mortgage was for that guaranteed rate of return. It’s essentially risk free! Compare that to a 0.4% APY “high yield” savings account and that 3.125% rate now looks pretty good! Based on my performance in the past three months, I should sell options with every dollar I have since my returns are so great, right?! Well, no. I’m not so naive to think that this will continue on forever without any losses.

All this to say that I will continue to remove my profits from my mortgage payoff trading account. I will continue to set aside the correct amount for taxes. Assuming I am left with more than my 1% goal for the month, I will take that 1% and put it towards my principal. The remaining balance is where I plan to… diversify.

Preferred Stock

I’m not going to take the time to explain the nuances of preferred stock here (Investopedia definition). It is often referred to as a hybrid of stocks and bonds. Anyway, I have been reading a book called Preferred Stock Investing and I believe there are some great opportunities for some fairly high yields. This month I actually bought two preferred stocks with dividends that yield an average of about 8%. I plan to take those dividends and put that money into the mortgage principal. Instead of taking my super high return from options trading and slowing it down immediately into my mortgage, these dollars will keep speed for a while longer.

While I expect (hope) to outperform even these high yields of 8% with my options trading, these income source has the benefit of being nearly completely passive. Options trading is one of the most active forms of trading, I am learning. Diversifying profits away from the options trading and into more passive income streams will help keep everything more sustainable as the account size grows.

Hedgefundie’s Excellent Adventure

Honestly, not really sure where to start with this. Think leverage. Think risk parity. That’s Hedgefundie’s Excellent Adventure. The strategy, specifically, is 55% in a 3X leveraged S&P 500 ETF $UPRO and 45% in a 3X leveraged long term bond ETF $TMF. Rebalance as required. There’s a great write up of the strategy here (it initially started from an epic thread on the “Bogleheads” forum).

After setting aside my portion straight towards the mortgage and purchasing any preferred stocks for the month, I will split my profits 55/45% into the Hedgefundie strategy. For now, my plan is to let this pile grow until I reach enough to reduce my mortgage term by one month. As of now, I need $643. This allows me to benefit from the great growth potential of leveraged ETFs while minimizing the risk since I won’t be letting it grow indefinitely.

So how did I slice this complicated pie this month?

After taxes ($53 into ULP), the $170 profits was $117 net. Instead of putting that $117 total into the mortgage as I would have in the previous two months, I put just $33, which is ~1% of my account’s starting principal of $3,240.86 for December. I bought two preferred stocks ($NRZ.A for $23.22 and $PMT.B for $24.75) for $48.15. Finally, I invested $36 into the Hedgefundie strategy, as $20 in $UPRO and $16 in $TMF.

With a combined $220 put towards my mortgage principal in three months, I will save $338 in interest over the life of the loan. In addition, my preferred stocks are now worth $49.55, a 4.2% return, and will yield ~8% going forward ($3.88 in dividends annually). Finally, the Hedgefundie’s Excellent Adventure is also up 4.2% to $37.53.

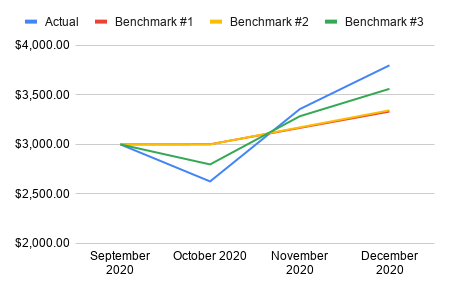

Benchmark Comparisons

In my introduction post I identified three different benchmarks I will be comparing my performance to. Benchmark #1 is putting all of my savings from my refinance, plus a 1 month skipped mortgage payment, into a savings account. When I wrote that post I was actually getting 0.6% APY, but it has reduced to 0.4%. Benchmark #2 is putting all of those savings straight into extra monthly payments to the mortgage principal. Finally, Benchmark #3 is simply buying $SPY.

I continued to make gains across all three benchmarks this month. When considering the value of my principal in my trading account + the monthly contribution of $64.21 and interest into my savings + the difference between the original loan and what is actually remaining this month, my total value is at $3,799 after the month of December, a 13.2% improvement over November. That beats Benchmark #1 (all savings) of $3,332 by 14.0%, Benchmark #2 (extra mortgage payments only) of $3,344 by 13.6% and Benchmark #3 ($SPY) of $3,561 by 6.7%. Below is a chart of my progress so far.

Thanks again for following along. Looking forward to more progress in 2021!

Disclaimer: I am long $AAL, $UPRO and $TMF.I am not a financial advisor. This is not investment advice. Please do your own research before investing in anything discussed herein. This post contains affiliate links.

According to this article (which I found via googling, “picking up pennies in front of a steamroller”, so take it with a grain of asphalt…), “The term `picking up pennies in front of a steamroller’ is linked to Nassim Taleb, an acclaimed author on randomness and risk, whose books describe an investment strategy that has a high probability to yield a small return (pennies), and a small probability of a very large loss (steamroller).”

I didn’t look further into what specific types of investments Taleb wrote about, but one clear example, at least through the lens of this blog, is writing puts and calls in options trading. We are collecting “pennies” at high probabilities, but once in a blue moon the “steamroller” is going to sneak up on us. Will all the pennies be worth it? Well, that of course depends on how shiny those pennies are and how many you pick up.

Let me tell you about how I just got steamrolled by over $1,100 while picking up $55 worth of pennies. The steamroller was $FCEL. I opened a position on FuelCell Energy on October 8 by purchasing 100 shares at $2.34. I then went on to sell multiple covered calls over the next couple of months at the $2 and $2.50 strikes, proudly picking up $10 to $15 at a time. With a $234 initial investment, each of those premiums represented a 4-7% return!

Things were looking just fine until mid November when the stock price shot up, way past my strike price. The price eventually reached over $10 (and over $13 today)! Had I not had that covered call position at $2.50 strike expiring December 18, I would have been up almost $800. A 336% return! Instead, I got my $55 worth of premiums and $16 in capital gains… a ~30% return.

Lesson Learned?

Well, the short answer is no, I didn’t learn a lesson here. I am still selling covered calls on positions. There is one thing I might do differently with these types of positions in the future.

$FCEL was a pretty speculative play. In fact, my original covered call was an in the money call at the $2 strike. I expected to make about a 6% return after selling for a capital loss and be done with it. I didn’t know if it was going to go up, down or sideways.

In the future, if I’m in a similar speculative play, I could potentially participate in the upside by buying “protection”: buying a cheap, long call at a strike price way out of the money. This would make my covered call a call credit spread. For example, if I had bought a call at the $4 strike, it probably would have only cost me a couple bucks. Sure, my return if the contract expires out of the money would have been those couple dollars less, but I could then have participated in the upside a bit. In this case, if I had a long $4 Call position, that would have been worth over $600 when the stock rocketed up past $10!

Here’s my update on Ford’s dividend: they’re still not giving one!

Since writing my post about creating my own dividend while I wait for Ford to resume theirs, I’ve done just that by selling covered calls on the position I already have in Ford. I have more than 200 shares currently, so I’ve been able to sell two contracts at a time.

Since writing that post, $F price went from $8.80s to almost $9.50 and now has pulled back down to nearly $9 again. We all know volatility is great for options sellers!

Here are the trades I’ve made and the current positions I have open:

Prior to writing that post, I actually had two open covered call positions on $F, one that was right at the money at $9 due to expire on November 20. Rather than risking the shares being called away, I closed that position and sold the December 24 $9.50 Call for a net credit of $.11. $.11 may not sound like a lot, but if that was a dividend payment, it would be the equivalent of an 11.5% yield! I used that credit to buy 1 share of $F for $9.00.

I had another $9 Covered Call position for December 18. I rolled that one out to January 15, this time keeping the $9 strike price. I took in a net credit of $.16 that time (11.9% annualized yield). Again, I reinvested that net credit by purchasing one share of $F at $9.10.

On December 3, I rolled the December 24 $9.50 out again to January 8 for a net credit of $.11 (10.7% annualized yield). I purchased one more $F at $9.26 with the credit.

On December 9, I rolled the January 15 $9 Covered Call (which is now pretty well in the money at this point), out to February 19 for a net credit of $.21 (11.3% annualized yield). I then purchased two $F at $9.43 with the credit. It’s unlikely $F will come down below $9 by February, but I will continue to roll this one out for as long as possible.

As the price of $F continued to tick up, I decided I wanted to try to roll out and up this time. I took that $9.50 January 15 covered call and rolled it out to February 19 for a net credit of $.08 (7.9% annualized yield). Since I didn’t get enough in credit for this one to buy another share of $F, I just pocketed the cash. However, it puts me in a great position to start selling covered calls at the $10 or higher strike price in the future.

Overall, I have taken in $67 of credits, less commissions, by doing this strategy over a fairly short time period. Let’s say that $67 was the quarterly yield amount for holding 200 shares of $F at the current trading price of $9.03, that would be equivalent to a dividend rate of 14.8% ($67 * 4 / (200 * $9.03) = 14.8%)!

Risks

I always want to be mindful of what risks I am taking. 14.8% yield sounds pretty good for a savings account, but of course, this isn’t in an FDIC account. This is real money that could be lost. With that said, before beginning options trading, I was OK with the risk of holding $F, at that point, because I thought the reward of the dividend payments and maybe some modest growth was worth it. In that case, I have no more risk than I had prior to selling these covered calls.

On the other hand, I have limited my upside potential. This isn’t a risk per se, but may make the risk I am taking less worth it. Some argue that option selling is the wrong kind of asymmetric risk… limited upside and unlimited downside (although in this case, the downside actually is limited because the stock can’t go below $0, but you get the point). To that, I would ask them would you rather be casino or the gambler? I’ll pick playing the casino every time. In addition, I’ve demonstrated that sometimes you are able to roll positions up to allow for even more upside from the stock. This is often an option so long as the stock hasn’t had an incredible run up in a short amount of time. And if it has, since I have been reinvesting my credits back into the stock, I still get to participate somewhat in that upside.

Conclusion

I do hope that Ford chooses to reinstate its dividend in 2021. There is still lots of chatter over at SeekingAlpha on when that might occur. However, as long as I am able to continue to roll out and, hopefully, up, I won’t be missing it much!

November was an incredible month for the markets. The S&P 500 rose 10.8% for the month and hit an all-time high. The Dow Jones’s 11.8% return for the month is the best single month since January 1987!

Because of my option writing (aka selling) strategy, my option trading returns weren’t able to beat the market. However, a large portion of some of my portfolios remain heavily invested in the markets, which keeps me from feeling too much FOMO and giving me the confidence to continue on with this strategy. I’m looking for lots of base hits here, from month to month. Over a long period, I think I can outperform the market, but only time will tell.

For the month of November, my profits from option trading were $2,114. That’s a total portfolio return of 2.3%, which is well below the S&P 500’s 10.8%. My total portfolio value across all accounts – which includes options trading profits, current stock & options positions, contributions & withdrawals for extra mortgage principal payments – was up 10.7%, inline with the markets. Contributions to these accounts were small this month, and $114 was withdrawn, so actual return is probably right around 10%. Remember that the markets were down 2.5% last month, and I generated options trading profits then, too. I closed 71 trades with a win percentage of 91%.

I continue to split my accounts between two strategies. One is to trade mostly credit spreads in margin accounts and the other is to sell cash-secured puts & covered calls (i.e. “the wheel” strategy) in non-margin and IRA accounts. The goal for the margin accounts continues to be to 1) raise cash to increase trading capital and 2) run through my mortgage pay off strategy. The other accounts are reinvesting the profits into stock positions for future growth or passive income via dividend stocks.

Last month almost half of my profits came from my margin accounts despite being just 11% of the total portfolio size. Many of my non-margin accounts had longer holding periods with expiration dates further out, so I realized a lot more profits in those accounts in November than I did in October. As a result, 84% of the profits came from the non-margin accounts this time. The margin account profits were a 3.7% return on total capital (43.1% annualized) and the non-margin profits were a 2.1% return (24.7% annualized).

10% is often cited as the historical annual performance of the S&P 500 since the 1920’s. Every month that I am beating that annualized return with options trading profits (and I crushed it this month with a combined 27.4% annualized return) and my total portfolio value is roughly inline with the overall market when it’s up (which I was within by about 1%), that’s a huge win. Just a couple years of this type of performance will have huge effects in my family’s longterm wealth creation. Let’s see if we can continue!

Biggest Winner

My best trade for the month in terms of profit was a wide Put credit spread on $FSLR. First Solar has been moving a lot over the last few months so the option premiums are really good. My original intent was to sell a cash-secured put (“naked put”), but decided I wanted to take some of the risk off the table so went with the spread instead. On November 13 I sold the $76 strike December 4 Put for a $2.04 credit and bought the $65 strike December 4 Put for $.35, giving me a net credit of $1.69 before commissions. When the stock moved up shortly after, I decided to close the position to lock in most of the profits on November 20. After commissions, I ended up with a profit of $130.36 on a 7-day trade which is an 11.9% return (541% annualized).

$FSLR chart from Stockcharts.com

With the initial credits I actually purchased 1 share of $FSLR for $80.30, which is now up 11.9% to $89.26.

Biggest Loser

My biggest realized loss was $52 on a Call credit spread on $SPY. On November 2 I sold the $348 strike December 2 Call for a $3.57 credit and bought the $349 strike Call for $3.26, for a net credit of $31 (commission free trades with Robinhood). This trade had a 74% chance of profit when I placed it, making the $31 possible gain with a $100 risk worthwhile. However, the market went way against me and I decided to cut my losses early on November 9 for a $52 loss. In hindsight it was the right move because the market just kept going and going, so I saved myself another $17 in potential losses ($100 risk – $31 credit – $52 loss = $17).

$SPY chart from Stockcharts.com

This trade was part of a strategy I coined “ETF Challenger” that I mentioned in previous posts. Essentially I am challenging the ETF to continue moving in the same direction when it made a greater than 1% move. So when $SPY is up more than 1% on the day, I sell a Call credit spread above it near the .30 delta (Investopedia: Understanding Position Delta). If it’s down more than 1%, a Put credit spread. I’m seeing just as many losers as winners on this, so I’m probably going to be ditching it going forward.

My biggest paper loss is actually much worse than $52. I sold the November 20 cash-secured Put on $GOLD at $27.50 for a credit of $.30. At expiration, the stock was trading down at $24.28, so I was assigned the 100 shares at $27.50 and immediately had a paper loss of $292 (+$30 – $2,750 + $2,428 = -$292). Unfortunately $GOLD has continued to pullback to $23.50 currently. I took in a small credit $7 credit for selling a December 18 $28 covered Call, which makes my current paper loss at $363 (+30 +7 – $2,750 – $2,350). I’m going to be patient with this one and continue to sell covered calls above my originally assigned price of $27.50. This position is in an IRA, so when I look at a horizon over many years I expect there to be an instance where I will want the hedge against the market in gold (while $GOLD is actually a mining stock, it generally moves in the same direction as the price of gold).

$GOLD chart from Stockcharts.com

Funding ROTH IRA

My last update for the month of November is that I finally funded a ROTH IRA! My wife and I are still under the household income limits for funding a ROTH, but I hope and expect that to no longer be true at some point in the future. I’m hoping to be able to fund that account with the maximum limit of $6,000 until we no longer qualify.

The obvious benefit of a ROTH over a traditional IRA is that future withdrawals are tax-free. Because of this, I’m hoping to create a stream of dividend income that can grow to a sizable amount at age 59.5. At that point, we will be able to take those dividend payments out each month/quarter and pay no taxes on them! For now, I’m planning to build the portfolio with REITs. My first trade: a cash-secured put on Realty Income $O, of course!

The second benefit I like about funding a ROTH is that, since contributions have already been taxed, they can be withdrawn at any age without penalty. It can essentially be used as a savings account where the principal is always available but the interest can’t be touched until age 59.5. My wife and I are keen on getting more involved in real estate, which means we will have a need for capital at some point in the future. By funding the ROTH rather than putting more money into a traditional IRA or regular 401k, we aren’t giving up control of that money for the next 30+ years.

I am very happy to report that my second month was even better than my first: $167 in profit! This is a 6.2% return on capital for the month of November (75% annualized).

Thanks to the overall market’s strong month, my long positions went up and I was able to completely reverse the 16% my principal was down. It is now at $3,240.86, which is 1.3% higher than the $3,200 I have added to the account thus far.

My positions & trades

$AAL, 109 shares at $13.98 ($1,523.73 total principal). Principal is currently up 2.3% ($34.97). I closed a total of four positions for a profit of $34. I currently have a $15 covered call position that I expect to collect another $34 from on New Year’s Eve.

$AAL November 2020 chart from StockCharts.com

$34 is a 2.4% return on my initial principal on American Airlines, well above my 1% goal each month, but much lower than the total portfolio’s returns of 6.2% for the month. The higher returns came from the other positions this month, but I’m happy to hold onto American Airlines for now. I think it will continue to move up and down with the COVID vaccine news, and I plan to ride that wave.

$FCEL, 100 shares at $2.34 ($233.78 total principal). At the close of November, Fuel Cell was trading at $10.18. That’s a 335% return! However, I sold a call option at $2.50, meaning my upside is limited to just $16, or less than 7%. Picking up pennies in front of a steam roller is a common metaphor used for selling options, and I think this is a perfect example of that. I plan to have a future post on this after it all shakes out. It will have a catchy title like, “How I missed out on $784.”

$FCEL November 2020 chart from StockCharts.com

As for the trades, I had a $2.50 call option that I collected $15 on due to expire on November 20. Rather than letting the shares be called away, I decided to roll the $2.50 to the next month for a net credit of $10 (the November contract was bought for $1.55 and the December contract was sold for $1.65). This is basically a guaranteed $10, or 4% return on the $250 principal I would collect if/when the shares are assigned. For me to lose money on this, the stock would have to retreat all the way back below my purchase price of $2.34. I am now so far in the money that I’m not sure I will be able to continue to roll the position for a profit. However, I will still try as long as I can get 2% or so.

$M, no open position. Macy’s is another stock that I missed some big upside gains on. However, I was able to milk it a little more than the $FCEL trade. I closed two trades for the month, netting me $54 on a position size of $617, which is an 8.8% return. When I finally had the shares called away at $6.50 on November 20, I profited $33 on the sale, but missed out on an additional ~$250 since the stock was then trading near $9. The stock is now above $10. I most likely won’t enter $M again unless there is a pullback.

$M November 2020 chart from StockCharts.com

$GPRO, no open stock position. Go Pro was my third position that was called away this month. I had 100 shares at $6.46, and the shares were called at $7 on November 6. You can see in the chart below that there was a big spike that I got caught in.

$GPRO November 2020 chart from StockCharts.com

In total I closed three trades for a net profit of $52. I currently have a $6.50 put due to expire this Friday, December 4. It is only an $8 credit, but that exceeds my 1% goal and was only a one-week contract. I expect to trade more cash-secured puts around the $6-$7 level going forward.

$APHA, no open stock position. Marijuana stocks are going nuts right now and option premiums are juicy. Aphria has been especially volatile due to a recently announced acquisition of Sweetwater Brewing Company. I currently have a $6.00 cash-secured put contract for December 11 that I collected a $17 credit on (2.8%). If I get assigned, I will sell a covered call in the $6.50-$7 range most likely.

$APHA November 2020 chart from StockCharts.com

Extra Mortgage Principal Paid

With $167 in net credits earned for the month, I am setting $53 aside for tax purposes. Last week I said I would be using $GNMA for my “tax escrow.” I have since been enlightened with the “The Ultimate Liquidity Portfolio” (ULP). I will have a forthcoming post on the idea as well as the book How to Stash that Cash by Chris Kawaja. In practice, the ULP can be implemented by putting 88% into intermediate term treasuries (e.g. $VGIT) and 12% in the US total stock market (e.g. $VTI). This puts my tax escrow account value at $99.82 as of this post.

So after taxes, I’m left with $114 that I decided to put directly towards my mortgage principal. With a combined $187 put towards my mortgage principal after two months, I will save $288 over the life of the loan.

Benchmark Comparisons

In my introduction post I identified three different benchmarks I will be comparing my performance to. Benchmark #1 is putting all of my savings from my refinance, plus a 1 month skipped mortgage payment, into a savings account. When I wrote that post I was actually getting 0.6% APY, but it has reduced to 0.4%. Benchmark #2 is putting all of those savings straight into extra monthly payments to the mortgage principal. Finally, Benchmark #3 is simply buying $SPY.

After losing to all three Benchmarks in my first month, I am now well ahead in all three. When considering the value of my principal in my trading account + the monthly contribution of $64.21 and interest into my savings + the difference between the original loan and what is actually remaining this month, my total value is at $3,356 after the month of November a 27.8% improvement over October. That beats Benchmark #1 (all savings) of $3167 by 6.0%, Benchmark #2 (extra mortgage payments) of $3,172 by 5.8% and Benchmark #3 ($SPY) of 2.2%. I’m pretty impressed that I managed to beat $SPY since November was the best month in the market in over 30 years.

I plan to put all these details onto my Using Options to Payoff My Mortgage Early page, including some tables and charts to show my progress from month to month. I’m still trying to format that so it’s easy to read, but hopefully I get that done before the end of the year!

Thanks for following along. I’m very happy with my progress, but it is just early days. Please don’t follow what I’m doing without doing your own research. Trading stocks and options can be risky. I hope you are inspired by these series of posts and my website to learn more about the strategies I am using to trade options and build wealth rather than attempting to follow blindly.

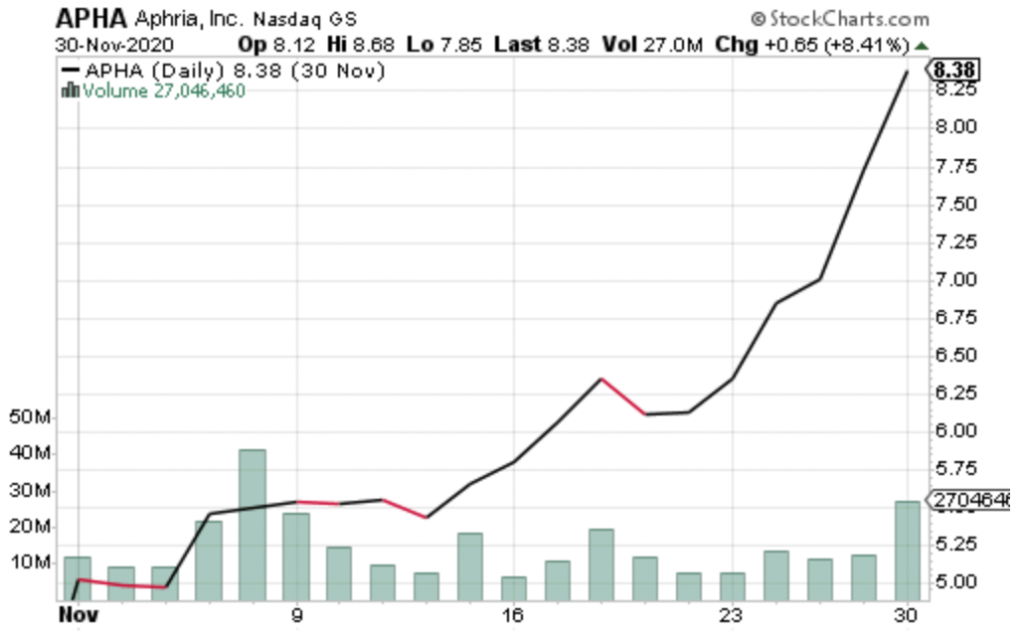

Almost immediately after the COVID-19 pandemic struck, Ford announced that it suspended its dividend. This was unfortunate news for me since I had been accumulating shares over the previous 6 months, having been allured by the 6%+ yield Ford was providing at the time in this yield-starved world we continue to find ourselves in. After wetting my lips with a couple tasty quarterly dividend payments (which I reinvested), the stock tanked from the $12 range to a 52-week low of $3.96 on March 23. I accumulated a few more shares here and there to lower my cost-basis, but without the promise of a dividend, my thesis on the company was broken. I wasn’t in it for the growth potential after all (most car companies that don’t end in “ESLA” have limited growth potential, in my opinion), I just wanted that dividend!

But then the stock started creeping back up as car sales proved to not go to zero as many feared during the varying levels of shutdowns we have seen throughout the US. Around this time I began trading options and immediately found an opportunity here with Ford. I began writing cash-secured puts below the market, using premiums earned to purchase shares and continue to lower my cost-basis, following the stock steady move up past $6, $7 and now $8. With my cost-basis now at $8.86, I’m nearly back to even with the stock closing at $8.75 at the close on Tuesday, November 17. I now find myself at a point where I can’t lower my cost-basis further by buying shares at the market price and I’m not interested in investing more capital, especially while there is still no dividend on offer. I still think there is a bit more upside to the stock, however, so I’m also not interested in selling at this point.

Creating my own dividend

I read this article on Seeking Alpha and was inspired to write this post. Rather than sitting on my hands while I hope that Ford resumes their dividend, I will be selling covered calls instead, essentially creating my own dividend. With my cost-basis at $8.86, I can now sell covered-calls at any strike price from $9 and above and still guarantee a profit in the event the shares get called away. I plan to sell the calls at least one strike price above the current trading price, as long as the premium I receive is above that 6% annual yield I was initially after. I would also like the credit I receive, less fees, to be more than the current trading price so that I can reinvest the credit just like I would with a standard DRIP.

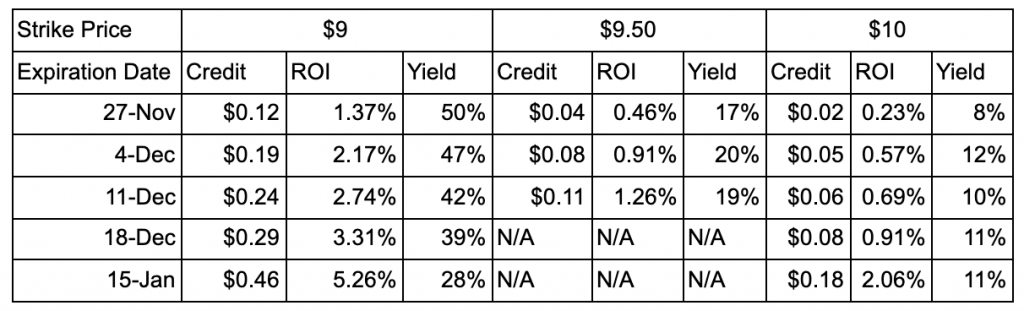

Below is a table of credits I could receive for selling calls at various strike prices and expiration dates. These credits are subject to market conditions, so they change constantly. However, they generally move up or down in unison, so I find this to be helpful in comparing my different covered call options.

With these data points known, I’m leaning towards selling the December 11 $9.50 call.

Downsides

Like any options trading strategy, there are risks and downsides associated. I’m going to briefly review some of them.

Stock drops

If the share price drops, I get to keep the credit I received up front, but my underlying shares of $F will have gone down. I got a return on my investment, but my principal is now diminished. I get to sell another call after expiration, hopefully at a still-attractive strike price/credit. This is still a risk even if I had not sold a call option and I was just waiting patiently for my dividend.

Shares get called away

If the shares go above my strike price, the shares will get called away at the strike price. Again I get to keep the credit I received up front AND I sell the shares for a profit since I picked a strike price above my cost-basis. If $F rips several dollars higher than my strike price, then I will have some FOMO for not getting to participate in the full upside. Such is the plight of option sellers.

Taxes

Besides losing some of the potential upside by writing a covered call, I am also increasing my taxable income with every option contract sold. I am doing these trades in a taxable account. If Ford was still paying a dividend, I would be collecting qualified dividends and therefore only being taxed as a capital gain (which 15% for my income bracket). Credits from option trading, however, are taxed as ordinary income (over 30%). While this is a factor to consider, I would rather pay taxes on income that I wouldn’t have had otherwise.