After a terrible month of returns in Month 9 (thanks to betting against $AMC!), I was able to right the ship a bit and post positive returns for July and August. The S&P 500 keeps humming along, however, and I’m now trailing the benchmark I’m measuring against of dollar cost averaging into $SPY.

In July a collected $157 in premiums (3.92% return on trading capital) and in August I collected $184 (4.51% return). In addition, at the start of September my trading capital is now back above the total contributions into the account ($4,108.52 vs total contributions of $4,100).

As I try to wrap things up for two months at a time, no detailed trade positions in this month’s update. I will say, however, I have a few PMCC’s (tastytrade description) open in $F, $MRO & $ZNGA; I continue to roll my $18-strike ITM covered call on $AAL; and I’m back to trading quite a few put credit spreads.

Beginning in July I got an exciting notice from my mortgage company that they have reduced my monthly escrow payment by $34.50, which increases my monthly contribution to $198.71 now! I’m excited to grow this into more returns.

Extra Mortgage Principal Paid

For July I made a major switch from putting a portion of my option trading profits for the month directly towards the mortgage. I now have several buckets going, with each bucket having its own strategy for deposits and withdrawals. I’m continuing with taking out 1% of my option trading account balance, but now that is going back into my money market account rather than directly towards mortgage principal. The balance in the money market then determines how much goes towards the principal, as well as 1/300th (4% annual) from my risk parity account and dividends from my preferred stocks. Lots of moving parts, but those following along know I’m not afraid of complexity!

For July’s principal payment, $1.04 came from my risk parity account (using 4% annual withdrawal rate); $.90 came from dividends paid from preffered shares; and $2.55 from my money market account (using account balance / CFI of mortgage payment); for a total of $4.49.

For August’s principal payment, $1.15 came from my risk parity account; $1.36 came from dividends paid from preferred shares; and $3.02 from my money market account; for a total of $5.53.

I have now paid an additional $455.16 towards the mortgage principal, which will save $692.91 in interest over the life of the loan.

Risk Parity

At the end of August, my risk parity style account was up to $346.11.

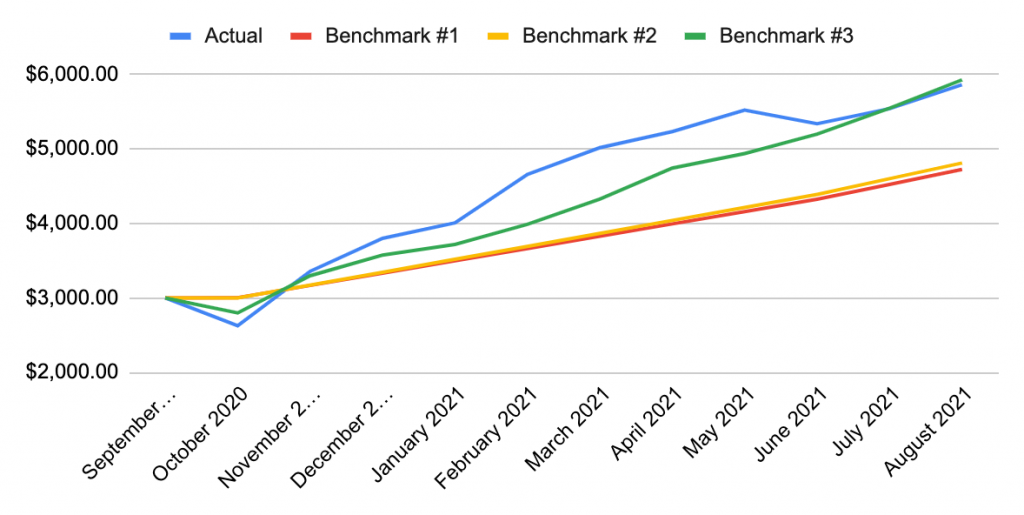

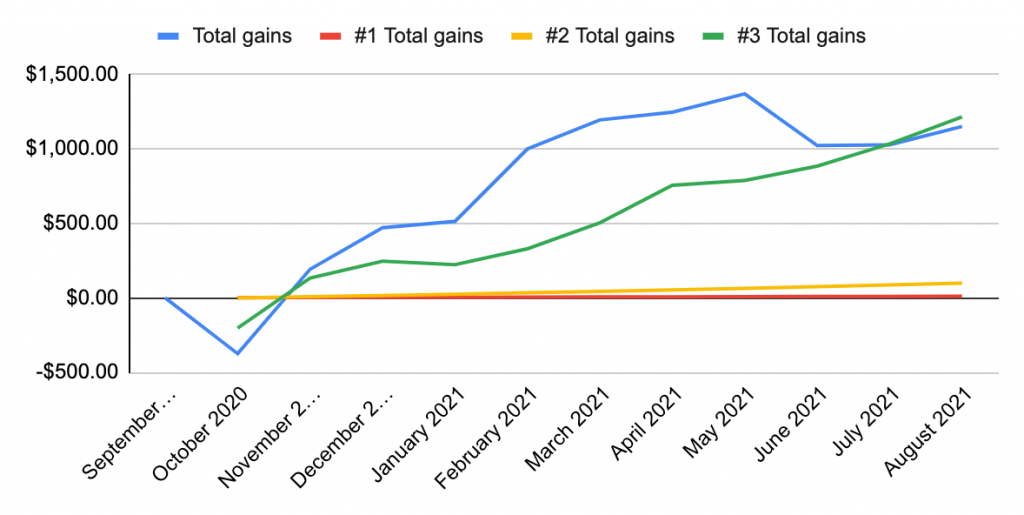

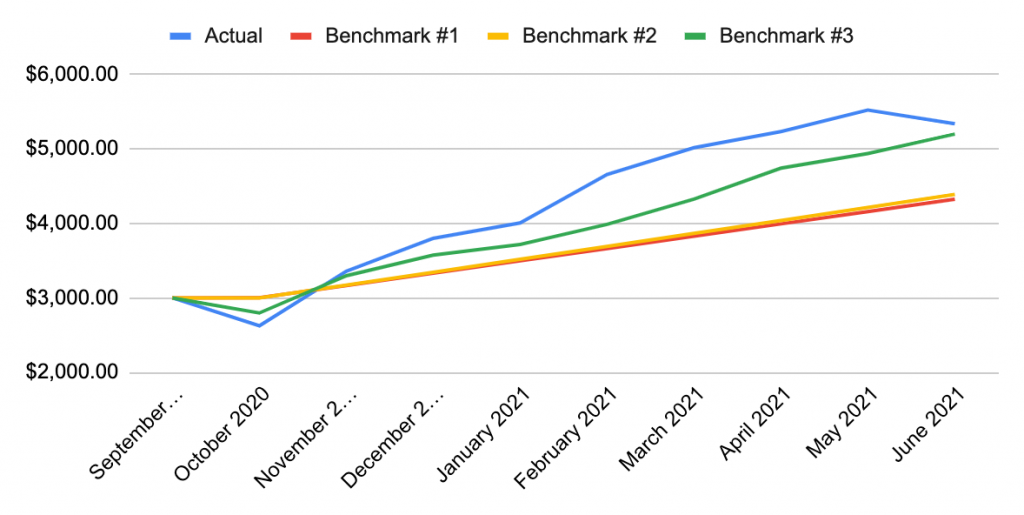

Benchmark Comparisons

In my introduction post I identified three different benchmarks I will be comparing my performance to. Benchmark #1 is putting all of my savings from my refinance, plus a 1 month skipped mortgage payment, into a savings account. When I wrote that post I was actually getting 0.6% APY, but it has reduced twice down to just 0.3% now. Benchmark #2 is putting all of those savings straight into extra monthly payments to the mortgage principal. Finally, Benchmark #3 is simply buying $SPY.

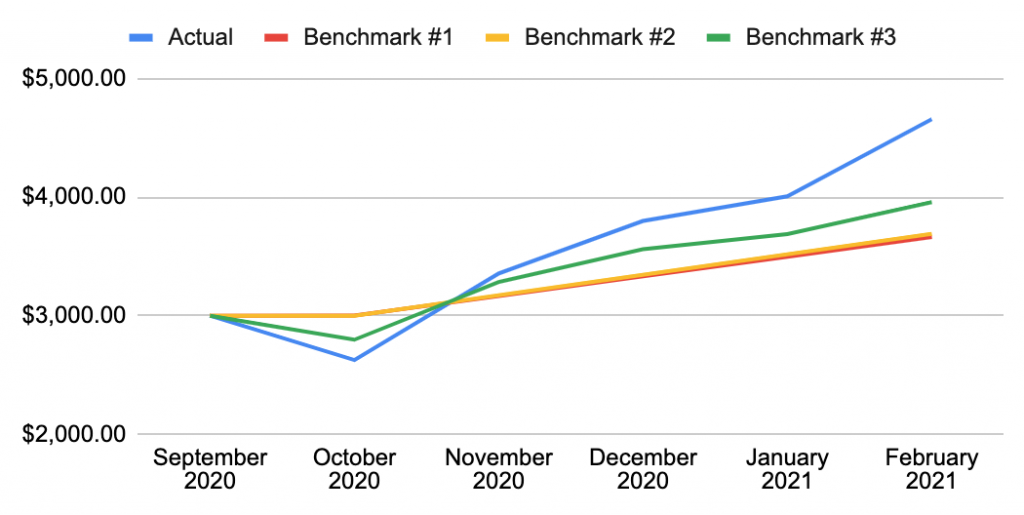

After 11 months I have invested $4,711.10 (initial $3,000 + $164.21 per month or $198.71 for months 10 & 11). Benchmark #1 is at $4,722.48, Benchmark #2 is at $4,809.61, Benchmark #3 is at $5,925.05. My actual total is at $5,860.53. Total return is now at $1,149.43, or 24.4% (26.9% CAGR). My returns include the value of my principal in my trading account + the principal in my money market account + balance of preferred shares + balance of risk parity account + the difference between the original loan and what is actually remaining this month. My results are beating Benchmark #1 by 24.1%, #2 by 21.9% and trailing #3 by -1.1%.

Despite finding lots of opportunities to collect premium in June, the month ended up being my worst on record thus far. The reason? I played a meme stock incorrectly. Specifically, $AMC. More details on that to follow, but first an update on the numbers…

I collected $230 in premiums, just shy of my previous record of $232.90 from March. Capital in my trading account reduced by $502 or -11.7%! As you will see below, this came about from that one bad trade and is a cautionary tale of the risk of destruction of capital when buying long option positions.

My positions & trades

Note: these summaries were written several weeks ago, but this post has sat unfinished in my drafts for a while

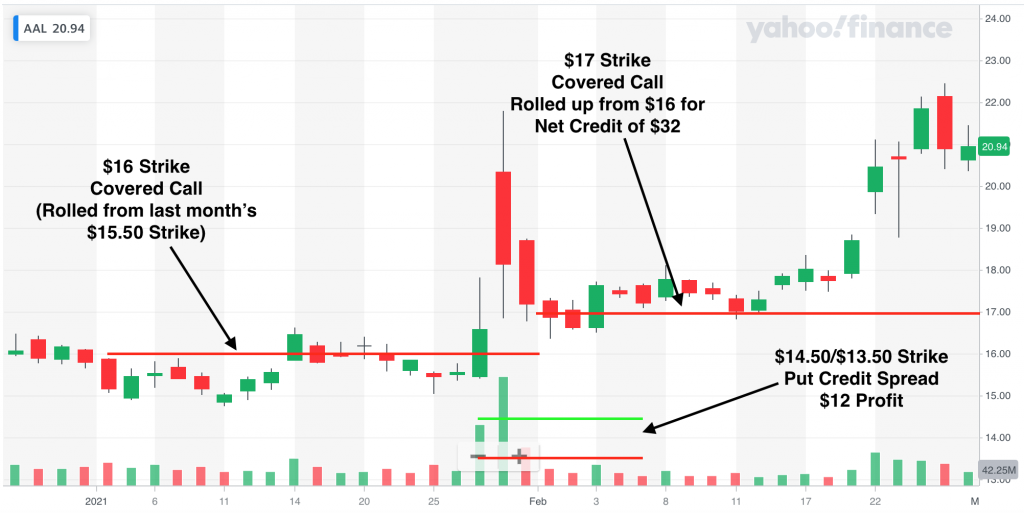

$AAL, 100 shares at $13.98 average ($1,398 total principal). As of the 1st of the month, my principal in American Airlines is up 51.7% ($723), however I am capped at a $402 gain due to a $18 strike covered call position expiring August 20 (I’ve already rolled it forward from July expiration to August for this month). I continue to be able to roll it forward for about a $20 profit, which meets my 1% goal. Since this is a classic covered call and not a PMCC, I plan to continue rolling this until I can’t collect a reasonable credit any longer.

$AMC, no current positions. So here is where everything went wrong! At the beginning of the month of June, $AMC started shooting up. When it was in the mid to upper $20’s, I decided to BUY an out of the money put at the $20 strike for August 20. I figured this was all nonsense and this would give me over two months to be right. Well unfortunately it continued up and the value of my long put tanked. I held the position for a while, but ultimately closed it for a $400+ loss in July (so technically the sale doesn’t belong in my June recap post) (also note, I wrote this recap on August ~11th, before it started to pullback into the $30s!).

To reduce the sting however, I did sell various puts that were essentially calendar spreads at the $20 strike that were shorter days to expiration than my long put due in August. For example, I sold the June 18 $20 strike put. Those added up to be $107.

While most people agree AMC is overvalued to say the least, I learned that it is difficult to play the direction correctly on these meme stocks. I think it is better to sell premium and most often with protection, like with credit spreads or perhaps even iron condors. I am trying this, for example, on $SPCE below.

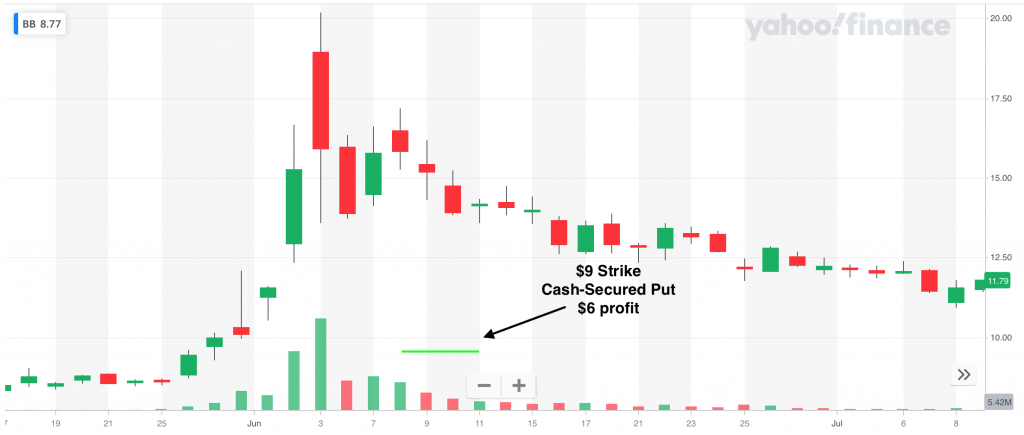

$BB, no current positions. This was another meme stock trade and more in line with how I think it is best to trade these stocks. I sold a $9 strike cash-secured put with 17 days til expiration. I collected a $13 premium which would be an annualized return of 29% for a .05 delta put! I closed the trade after just a few days because I was profitable and the stock was moving against me. I was essentially wrong about the direction of the trade, but was right on the change in volatility. Had the stock continued to go up and not down, I likely would have held a bit longer and to squeeze out a bit more premium.

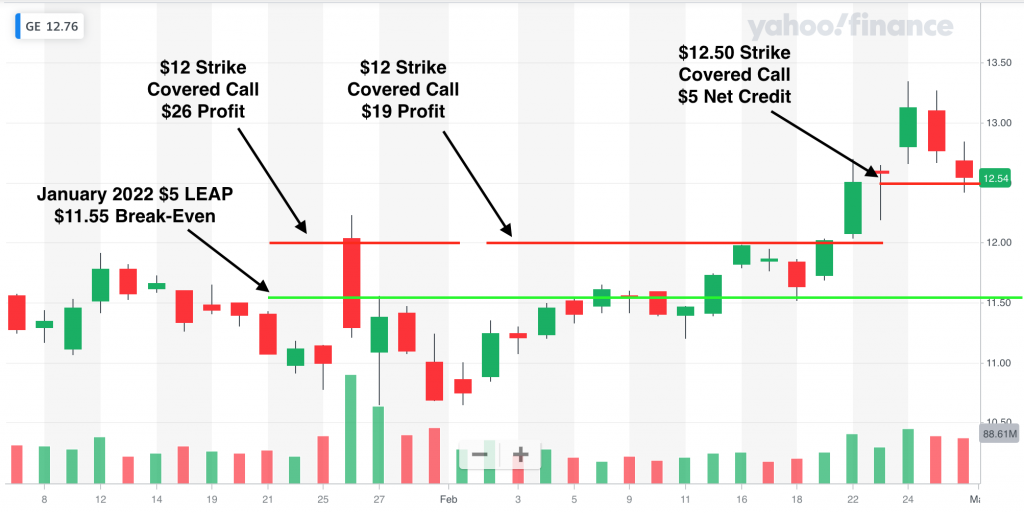

$GE, 1x LEAP January 21, 2022 $5 Strike Call at a cost of $6.55; 1x July 23 $12.50 Covered Call. Nothing too exciting here. I rolled my June expiration covered call forward to July for a net credit of $20, which is a 2.7% return (26.3% annualized). GE has been hovering in this $12.50 to $14 range. Since my long leg is now less than 6 months until expiration, I am considering letting this expire in the money and allow the LEAP to be called away.

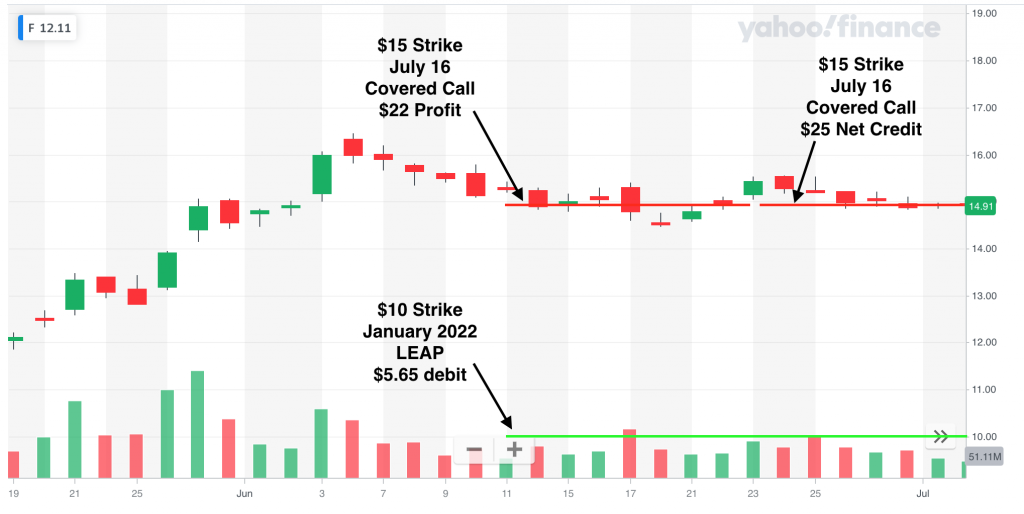

$F, 1x LEAP January 21, 2022 $10 Strike Call at a cost of $5.65; 1x July 30 $12.50 Covered Call. I like trading Ford options because there is a ton of liquidity. I actually sold my short leg initially ITM at $15 when it was trading in the $15.50 range. This proved to be the right call as we’ve seen a strong pull back in Ford. I wish I had gone with a longer expiration on the LEAP of at least 12 months. We will see how this turns out.

I did roll my initial ITM covered call from June to July expiration when the stock dropped near my $15 strike. There is always an increase in premium when this happens and I’ve found it to be a good time to roll out if possible. I earned $22 profit on the first trade (It was actually $87 but because I sold this one ITM I am doing some financial engineering to make my LEAP at an actual cost of $500. This way if I get assigned on my $15 strike, I don’t need to count the LEAP being called away at $5 as a loss.).

$SNDL, 100 shares at $1.58 average ($158 total principal); 1x $1.50 July 16 covered call. Judging by the current share price of under $1, this is looking like a pretty poor trade. However, I have been able to grab $7 to $8 credits each month for selling at $1.50 strike. This

$SPCE, 1x $25/$20 Strike August 20 Put Credit Spread. After my little AMC debacle I wanted revenge! But didn’t want to dig myself a bigger hole, either. As mentioned above, I think credit spreads may be the best way to go about these meme stock trades. My reasons are defined risk (equal to the risk of the spread, i.e., $500 on this position) and the long position is a hedge against the possibility of increased volatility. Just when you think the implied volatility for these type of stocks can’t go any higher, and you’re tempted to open a short option position, things get even crazier and you can be left way underwater on the position, even if you aren’t actually in the money. The long position helps limit this because while the short leg is increasing in value, so too is your long leg, albeit not by quite as much. I opened this position for a credit of $50, which would be a nice 10% gain! However, I will likely close the position if I can get a 50% gain or so.

Extra Mortgage Principal Paid

In June I began to have some real changes of heart in terms of how I was going about paying down this mortgage. While I am not shying away from the idea of paying off mortgage debt, I clearly feel that there are better ways to go about this rather than just paying extra principal every month. My results thus far speak for themselves, as I’m up over a $1000 pursuing my current strategies rather than just chucking away my extra cashflow towards the mortgage principal (“Benchmark #2”).

Recall that my latest idea was to put 1% of my monthly option trading profits towards the mortgage. Anything over would go towards buying preferred stocks or “Hedgefundie’s Excellent Adventure.” But even that 1% seemed like too much. Surely this can be optimized further. (even if that comes at the cost of complexity, which I clearly don’t have any aversion to!) Enter Cash Flow Index…

As I’m writing this I’m realizing all this belongs in its own post (or series of posts), so I will get straight to the point. Cash Flow Index is a way of quantifying the efficiency of a debt.

CFI = (Loan Balance) / (Monthly Payment)

If the debt is large but only requires a small monthly payment (like the early stages of a mortgage), it is efficient and has a high CFI. Conversely, if the debt is relatively small but requires a larger debt payment (like the late stages of a mortgage), it is less efficient and therefore might make more sense to pay off. The longer the amortization schedule, the more efficient. A 5 year car loan? Not so efficient. I like CFI because it balances out some of the effects of interest rates and duration of the loan on your debt payment.

My CFI for my mortgage after June’s payment was 230.1 ($503,051 / $2,186 = 230.1).

With that in mind, I’m toying with ways of incorporating that into my extra mortgage payments. For the month of June, I decided to divide the principal balance in my trading account by the CFI. This came out to about $19 ($4,310.44/230.1 = $18.73). As I get closer to paying off the mortgage, the amount that will go towards the principal will accelerate. 230.1^-1 is 0.43% (5.2% yearly). When the CFI is down to 100, which currently is month 243, that would mean 1% monthly will go towards the principal.

My preferred stock portfolio paid $1.72 in dividends and I “withdrew” $1 from my new risk parity portfolio (formerly Hedgefundie… read below), for a total of $21.72 towards mortgage. I have now paid an additional $445.14 towards the mortgage principal, which will save $678.06 in interest over the life of the loan.

The portfolio formerly known as “Hedgefundie’s Excellent Adventure”

I decided to switch my Hedgefundie strategy to a more classic risk parity style portfolio. Risk parity portfolios use a mixture of equities, bonds, gold, commodities, CEFs, REITs, etc. Depending on the mixture, they can often have equity-like returns with much lower volatility. More on this to come in another post, but for now I’m using a mixture that heavily weights equities and uses leverage. Just not quite as much as Hedgefundie’s Excellent Adventure! I plan to take a 4% yearly withdrawal (i.e., 1/300th of the portfolio value each month) to go towards the mortgage principal. However, I’m still making deposits from my option trading so I will reduce that deposit net of the required 4% withdrawal for the month. At the end of the month the portfolio was at $267.16. I just rounded the net withdrawal up to $1.

Benchmark Comparisons

In my introduction post I identified three different benchmarks I will be comparing my performance to. Benchmark #1 is putting all of my savings from my refinance, plus a 1 month skipped mortgage payment, into a savings account. When I wrote that post I was actually getting 0.6% APY, but it has reduced twice down to just 0.3% now. Benchmark #2 is putting all of those savings straight into extra monthly payments to the mortgage principal. Finally, Benchmark #3 is simply buying $SPY.

After 9 months I have invested $4,313.68 (initial $3,000 + $164.21 per month). Benchmark #1 is at $4,322.85, Benchmark #2 is at $4,388.79, Benchmark #3 is at $5,197.40. My actual total is at $5,335.53. June was my first month since month #1 that had a negative return. Total return is now at $1,021.85, or 23.7% (32.8% CAGR). My returns include the value of my principal in my trading account + the monthly contribution of $64.21 and interest into my savings + the difference between the original loan and what is actually remaining this month. My results are beating Benchmark #1 by 23.4%, #2 by 21.6% and #3 by 2.7%.

My last month was my worst yet in terms of option premiums collected in my quest of paying off my mortgage early. I still was past my initial goal of 1% collected for the month, however, with 1.7% for April. I think my first few months of 5%+ returns was mostly luck and not sustainable, so not surprised to see my performance comeback down to Earth a bit.

May was better than April with $125.75 of premiums collected which is a 2.9% return. Capital grew to $4,310.44, which is a .6% increase over April after excluding the $100 deposit into my trading account. At the risk of falling further behind on these update, no updates on my current positions and trades for May.

Extra Mortgage Principal Paid

As I explained in January’s post, I don’t take my options trading profits and put all of it towards the mortgage anymore. Instead I spread it across a couple other investments that I think are very likely to beat my 3.125% mortgage APR in the long run. I now target just 1% of the beginning trading portfolio value each month. May started with a value of $4,186, so I rounded 1% up to $42.

My preferred stock portfolio also paid out a few dividends as well as taking some capital gains from selling some shares and reinvesting in cheaper preferred shares. This amounted to $3.97 net, bringing the total paid towards the mortgage of $45.97. I have now paid a total of $423.42 over the past eight months towards my principal, which will save $645.66 over the life of the loan.

Preferred Stock

My first passive alternative to directly paying off my mortgage principal is preferred stock. At the end of May, my preferred stock portfolio for this mortgage pay off strategy was worth $296.69 and consisted of eight different positions. I purchased one preferred stock ETF for the month, totaling $24.45.

I hope to have a complete update with my benchmark numbers and an update on Hedgefundie’s Excellent Adventure next month!

Recap: In my fifth month (February) I had my fifth consecutive record-setting month of option trading profits, posting up $199 and increasing the principal in my trading account to $3,964.77. In total, I had paid a total of $293.33 extra principal towards the mortgage, which will equal a total savings of $450 over the life of the loan. In total across my four diversified strategies, I had earned a return of $999.43 on my $3,656.84 total investment, which is 27.7% or a CAGR of 78.6%. Read my initial post for a background on this strategy.

I missed the March updated post and, at the risk of falling too far behind, I’m going to update on both March and April in this post. I will skip the positions and trades piece of the post as that takes the most time to create.

March was another killer month with a $232.90 in profits, which was a 5.7% return on principal. Account principal stood at $4,102.97 at the end of the month. April was much more modest at just $72.65, a 1.7% return. This was still enough to cover my 1% goal to paying down mortgage principal. My principal in the account at the conclusion of April is at $4,186.37.

Extra Mortgage Principal Paid

In March, my 1% withdrawal towards the mortgage was $40 (1% of $3,964.77 rounded up to $4,000). I received $1.71 in preferred stock dividends, so $41.71 was applied to the mortgage.

In April, my 1% withdrawal is $42, plus $.41 in preferred stock dividends, totaling $42.41.

After April’s payment, I will have paid $377.45 over seven months, which will equal $576.80 of interest savings over the life of the loan.

Preferred Stock

My first passive alternative to directly paying off my mortgage principal is preferred stock. At the end of April, my preferred stock portfolio for this mortgage pay off strategy is worth $270.08 and consisted of nine different positions. I purchased three preferred stocks in March (none in April), totaling $68.77. Here are my current holdings:

SCE-J (2 shares), 5.375% coupon with a yield on cost of 5.57%

Hedgefundie’s Excellent Adventure

This strategy is purely for capital growth. The target allocation is 55% UPRO/45% TMF, which are both 3x leveraged ETFs. Once their value is enough to reduce my mortgage term by one month, I will put it all towards the mortgage and start over. My current balance is quite skewed towards UPRO at 65.3%, but I just don’t feel good about buying more of a leveraged longterm US treasury fund with the threat of increasing interest rates. Instead, I have chosen to make future buys at 50/50. In April I bought $4 of UPRO and $4 of TMF. My excellent adventure is now valued at $142.61, which is a positive return of 8.9%. To reduce my mortgage by one month I would need to make a $491 payment. I would like to reach that point before the end of the year, but will need some bigger months in the future to make that happen.

Benchmark Comparisons

In my introduction post I identified three different benchmarks I will be comparing my performance to. Benchmark #1 is putting all of my savings from my refinance, plus a 1 month skipped mortgage payment, into a savings account. When I wrote that post I was actually getting 0.6% APY, but it has reduced twice down to just 0.3% now. Benchmark #2 is putting all of those savings straight into extra monthly payments to the mortgage principal. Finally, Benchmark #3 is simply buying $SPY.

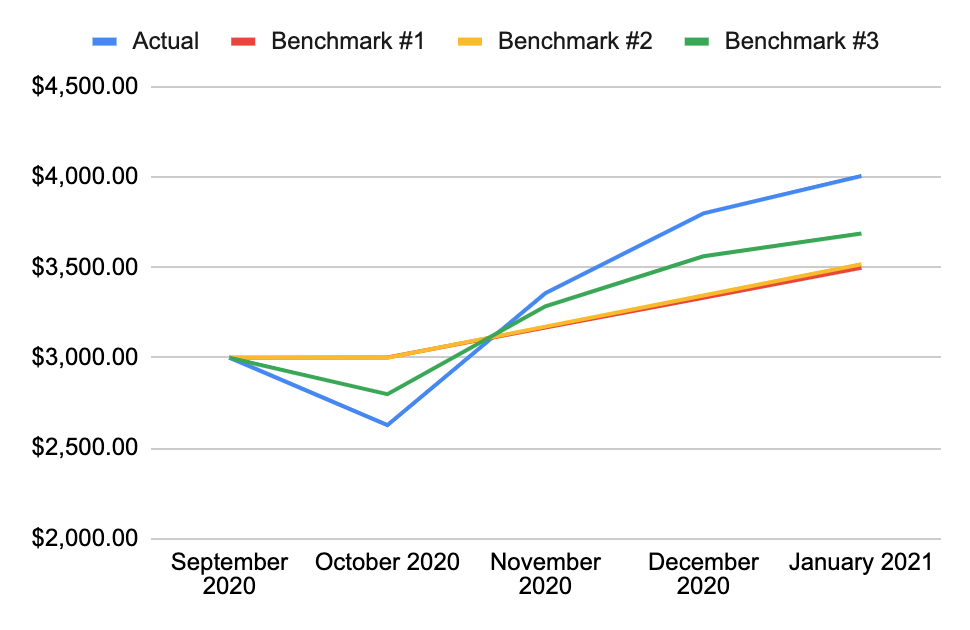

After 7 months I have invested $3,985.26 (initial $3,000 + $164.21 per month). Benchmark #1 is at $3,992.40, Benchmark #2 is at $4,038.88, Benchmark #3 is at $4,693.75. My actual total is at $5,229.91. Total return is now at $1,244.65, or 31.2% (59.4% CAGR). My returns include the value of my principal in my trading account + the monthly contribution of $64.21 and interest into my savings + the difference between the original loan and what is actually remaining this month. My results are beating Benchmark #1 by 31%, #2 by 29.5% and #3 by 11.4%.

Recap: In my fourth month (January) I had a record-high option trading profits of $188 in my mortgage pay off strategy, however my principal in the trading account barely grew and sat at $3,515.08. In total, I had paid a total of $256 extra principal towards the mortgage, which will equal a total savings of $393 over the life of the loan. In total across my four diversified strategies, I had earned a return of $513.33 on my $3,492.63 total investment, which is 14.7% or a CAGR of 50.9%. Impressive numbers, and way beyond my initial goals. And most certainly not sustainable! (If it were sustainable, I will be opening my own hedge fund by the end of this.)

Thanks in large part to beginning to implement some synthetic covered calls (aka “poor man’s covered call” or “PMCC”) and some luck in timing the market, February was another record-setting month. I earned $199 in options trading profits, a 5.5% return on capital and another record! I was able to grow my principal up to $3,964.77 which is 13.3% more than the previous month. More details on the breakdown of profits across the four strategies below, but first my positions and trades…

My positions & trades

$AAL, 100 shares at $13.98 average ($1,398 total principal). Principal is now currently up an astounding 51% ($713.08), however I am capped at $17 due to a $17 strike covered call position expiring March 19. Therefore, my capital gains are limited to just $302 total. I closed two positions for the month and for a profit of $39 (one put credit spread and one covered call). Similar to last month, I collected a net credit of $16 after rolling up from a $16 strike position to the current $17 position.

I have yet to decide whether I will try to roll up again or just out to April, assuming I can get an acceptable return. American Airlines is now getting to a point where I think it doesn’t have that much more upside from the county reopening. Basically, I think all of that is already priced in. For that reason, I am leaning toward rolling to another $17 strike. Implied Volatility remains high, so I should be able to get a decent return for that.

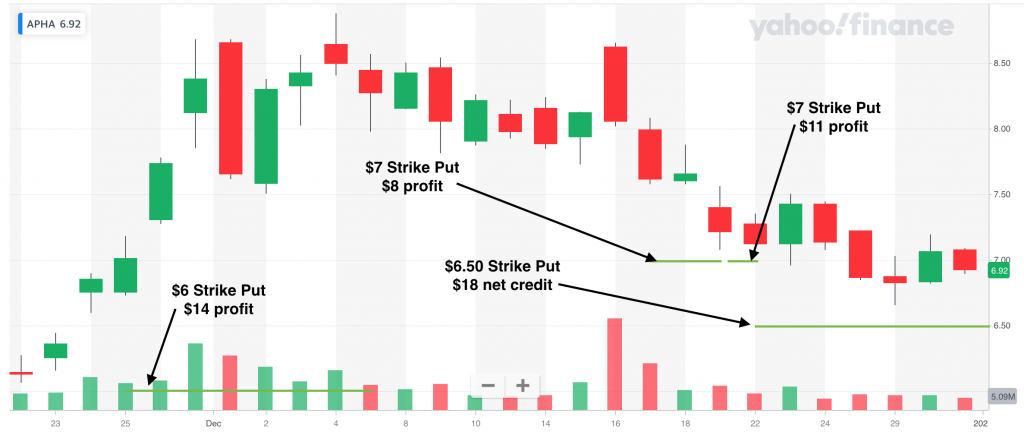

$APHA, no open positions. This month I traded two put credit spreads on Aphria. It’s had quite a run up, so was able to close both out for profit. Downside of selling puts is that the maximum profit is capped. When you have incredible run-ups like $APHA did it’s hard not to have FOMO. Still, ROI on these was nothing to complain about. The two trades totaled $43 in profits. With $100 at risk over the course of 14 days is an annualized ROI of 112%!

$GE, 1 LEAP January 21, 2022 $5 Strike Call at a cost of $6.55; 1 March 26 $12.50 Covered Call. As I wrote last month, I am trying synthetic covered calls (aka “poor man’s covered call” or PMCC) for the first time. Both of my trades are going really well. With $GE trading at $12.54 now, that $5 strike LEAP is now worth $7.55, which is a $100 profit right now. In addition, I closed two covered call positions during February for $45 total profit. Those covered call positions were at the $12 strike. I rolled the second one up to the current March 26 $12.50 strike covered call for a net credit of $5.

If my covered call gets assigned at $12.50, my $5 LEAP will be forced to be exercised and the spread will be what I take home. So $750 here. For that reason, when calculating my total principal, I cap this position at $750 (unless I roll it up to a higher strike).

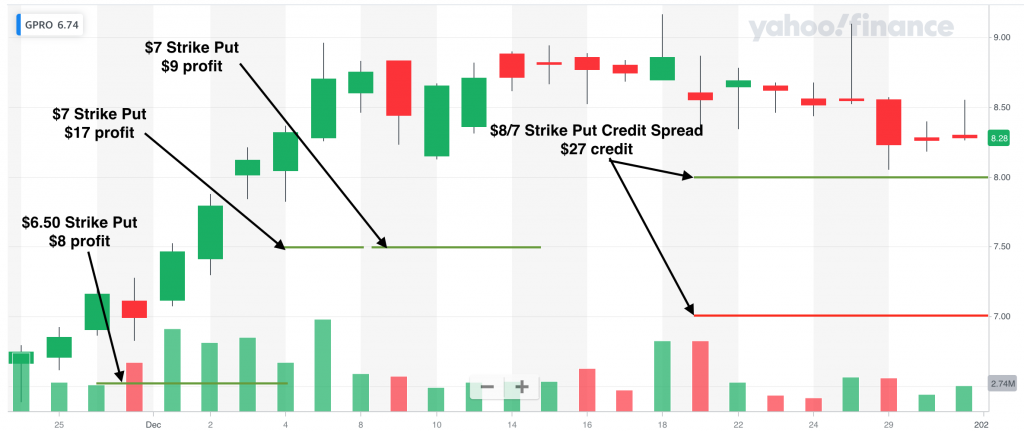

$GPRO, no open stock positions. I only had one trade on Go Pro in February, a $1 wide put credit spread. I opened the $8/$7 strike position after the stock had dropped considerably. I actually was wrong on the direction of this trade, as the stock continued to go below my short strike, as shown in the chart below. Thanks to theta (time decay) and vega (reduction in volatility), this one was on the side of the option seller. I closed the position for a small, $6 profit. This month I have sold some cash-secured puts at $7.50 strike.

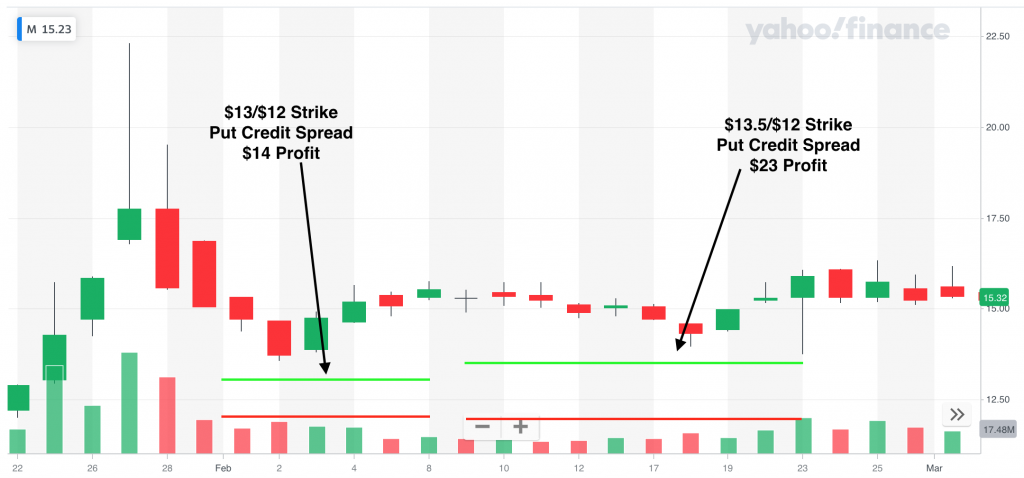

$M, no open positions. I continued from last month selling put credit spreads on Macy’s. The premiums were good and the volume was also good making spreads more attractive. I find it hard to get orders filled for spreads on the less liquid stocks sometimes. I closed two trades for a total profit of $37.

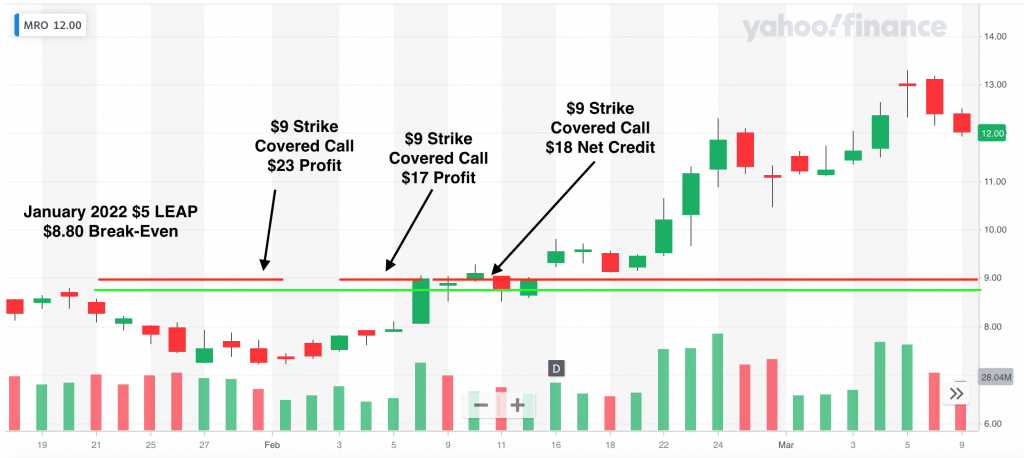

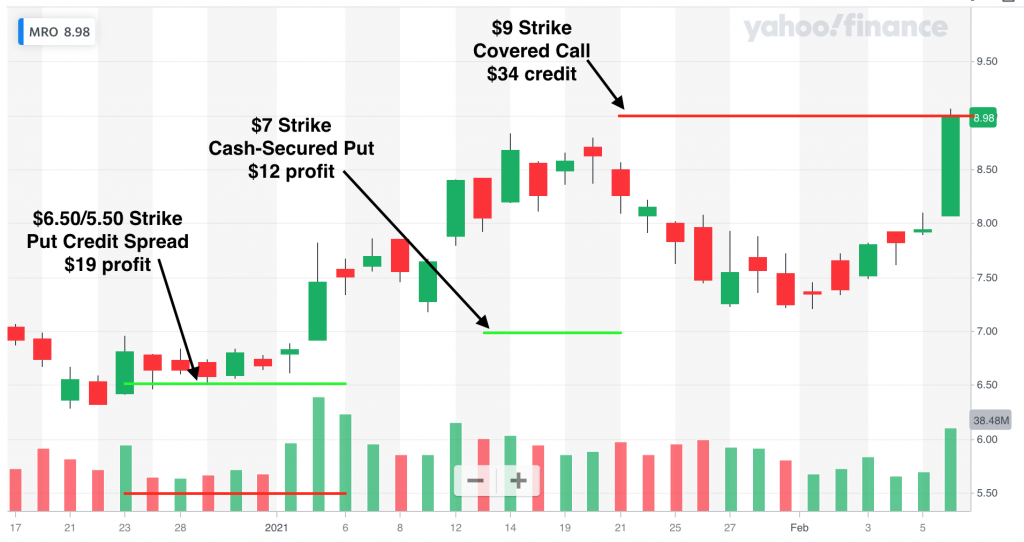

$MRO, 1 LEAP January 21, 2022 $5 Strike at a cost of $3.80; 1 March 12, 2021 $9 Covered Call. Last month I said I was going long on Marathon Oil Corporation because I thought demand for oil would increase as the World begins to open up from COVID-19. Well, I was right. Gas prices are up and $MRO has blown past my $9 strike! At over $12 it is now basically at pre-pandemic levels.

I closed my first covered call for a nice $23 profit. But then I should have moved the strike up to $9.50 so I could have had a little more appreciation. However, I was still able to make $17 on my next covered call when I rolled it out to my current contract. Unlikely that I will be able to continue collecting good premiums on this so I might have to let this one go in March.

Extra Mortgage Principal Paid

As I explained in January’s post, I don’t take my options trading profits and put all of it towards the mortgage anymore. Instead I spread it across a couple other investments that I think are very likely to beat my 3.125% mortgage APR in the long run. I now target just 1% of the beginning trading portfolio value each month. February started with a value of $3,514, so I rounded 1% up to $36.

In addition, my small but growing portfolio of preferred stocks paid out their first dividends, which totaled $1.33. So between the two, I put $37.33 towards the mortgage. I’ve now paid a total of $293.33 over the past five months, which will equal $450 in savings over the life of the loan.

Preferred Stock

My first passive alternative to directly paying off my mortgage principal is preferred stock. At the end of February, my preferred stock portfolio for this mortgage pay off strategy was worth $187.01 and consisted of seven different positions (8 shares total). I purchased three preferred stocks for the month, totaling $67.31. Here are my current holdings:

SCE-J (2 shares), 5.375% coupon with a yield on cost of 5.57%

February’s $1.33 in dividends came from $NRZ-A, $NRZ-B and $CDR-C.

Hedgefundie’s Excellent Adventure

This strategy is purely for capital growth. The target allocation is 55% UPRO/45% TMF, which are both 3x leveraged ETFs. Once their value is enough to reduce my mortgage term by one month, I will put it all towards the mortgage and start over. I have yet to rebalance this because the total value is still so small, but rebalancing is critical to this strategy’s success. For February, $15 was put into $UPRO and $17 into TMF. At the end of the month, the value in these funds was $88.01, which is actually a negative return on the $93 I’ve invested. Nothing to sweat at this point, I will just continue to buy more at lower prices. To reduce my mortgage by one month I would need to make a $573 payment, so still a long way to grow.

Accounts Summary

Of the $199 earned from options trading in February, $62 was set aside into the ULP for taxes, $37.33 was put towards the mortgage principal, $67.31 was invested into preferred stocks and $32 was invested into Hedgefundie’s Excellent Adventure. The remaining $3.02 will stay in my trading account. The trading account’s value ended January at $3,964.77, preferred stock was at $187.01 (with a forward yield of 7.35%) and Hedgefundie was at $88.01.

Benchmark Comparisons

In my introduction post I identified three different benchmarks I will be comparing my performance to. Benchmark #1 is putting all of my savings from my refinance, plus a 1 month skipped mortgage payment, into a savings account. When I wrote that post I was actually getting 0.6% APY, but it has reduced twice down to just 0.3% now. Benchmark #2 is putting all of those savings straight into extra monthly payments to the mortgage principal. Finally, Benchmark #3 is simply buying $SPY.

After 5 months I have invested $3,656.84 (initial $3,000 + $164.21 per month). Benchmark #1 is at $3,662.10, Benchmark #2 is at $3,690.78, Benchmark #3 is at $3,957.27. My actual total is at $4,656.27. I’m just shy of $1k total return at $999.43, or 27.3% (78.6% CAGR). My returns include the value of my principal in my trading account + the monthly contribution of $64.21 and interest into my savings + the difference between the original loan and what is actually remaining this month. My results are beating Benchmark #1 by 27.2%, #2 by 26.2% and #3 by 17.7%.

The market has had plenty of ups and downs the past couple months. I will keep plugging away and hopefully will be able to continue to outpace all three benchmarks!

Disclaimer: I am long $AAL, $MRO, $GE, $CDR-C, $GLOP-A, $NRZ-A, $NRZ-B, $PEB-C, $PMT-B, $SCE-J, $SPY, $UPRO and $TMF. I am not a financial advisor. This is not investment advice. Please do your own research before investing in anything discussed herein.

It’s been two months since my last update on my covered call strategy on $F while I wait for a dividend to be reinstated. As outlined in my first post, the ~6% dividend Ford was offering in 2019 was the primary reason I started accumulating shares. With the COVID “crash” in March the dividends were “suspended” while the company stabilized. That was probably the correct move for the company’s longterm future, but that doesn’t mean I didn’t miss those quarterly payments!

With that in mind, I started selling covered calls at strike prices above my average price to generate some income on that tied up capital I had in Ford. As the share price has rebounded, I have found myself in the money on my positions, but I have still been able to roll them out for an acceptable rate of return.

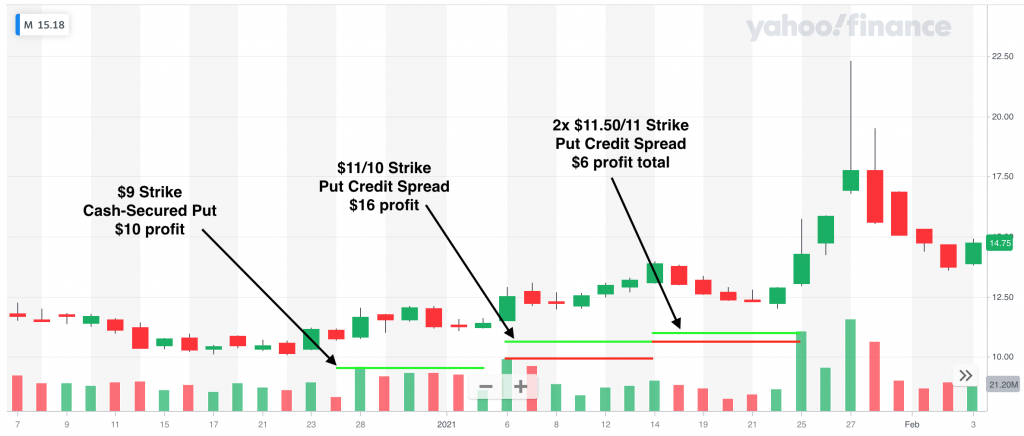

As of my last update, I had two February 19 covered calls, one at $9 strike and $10 strike. I had taken in $67 in credits before commissions. $F is now trading in the mid-$11s. Since then, I have been able to roll both of those out to March for another credit.

On January 22, I rolled the $9 covered call out to March 19 for a net credit of $16.68. This is a 1.9% return over 57 days, which is 11.9% annualized. With that credit, I bought one additional share for $11.47. This is similar to a DRIP (Dividend Reinvestment Program) with a traditional dividend.

On February 2, I was able to roll the $10 covered call out to March 19 expiration for a net credit of $31.68. This is a 3.2% return of 46 days, which is 25.1% annualized! As of now, I haven’t reinvested that credit and have just kept the cash.

This brings the total net credits from selling covered calls to over $115. At a current share price of $11.58, that’s a return of 5% over the course of about 3 months.

These positions, especially the $9 strike, are sitting pretty far in the money at this point. This means that there is very little extrinsic value remaining in these contracts, which means sooner or later I will choose to let it expire at have the shares called away. Fortunately, I have more than 200 shares of $F that I’ve own for more than 1 year, so my gains on those shares will be taxed at longterm capital gains if I’m forced to sell when they’re called away (to be clear: all the credits I’m receiving for selling the covered calls are taxed as ordinary income, unfortunately). If the stock price sees a pullback down below $11 again, I will look at rolling these out again as it’s likely there will be some more extrinsic value again. As long as I can get a 1% net credit for rolling out between 1 to 2 months, I think it will still be worthwhile as that’s a 6-12% annual return that, I feel, is pretty low risk.

I do expect Ford to resume the dividend at some point, so it would be nice if I could continue to roll out until then. But if Ford continues to climb higher and I get further and further in the money, that becomes increasingly unlikely. Either way, I will continue to update the blog with what happens.

Disclaimer: I am long $F. I am not a financial advisor. This is not investment advice. Please do your own research before investing in anything discussed herein.

The market in January had a strong start before Game Stop mania threw a wrench into things. I actually participated in the craziness in a very small way. I sold a call credit spread that was WAY in the money for a few days (like… $300 in the money!) Since it was a defined risk trade I had no problem waiting it out. In the end I was probably the only person on that $GME trade that ended up with a $10 profit. I think most were were up or down 100x, 1000x or more than that. As the dust began to settle, $SPY retreated a bit and closed the month down 1.0%.

My total profits from trading were $2,623.63, another best ever month by 13%! That was a 1.5% total portfolio return from options trading. Not bad for a month where the markets were in the red. My total portfolio value across all accounts – which includes options trading profits, current stock & options positions, contributions & withdrawals for extra mortgage principal payments – was up 0.6%. I did contribute $6,000 into my ROTH IRA in January, but that isn’t included in the returns for the month. In January I closed 71 trades with a win rate of 96%*.

(* That win rate is a bit misleading because it doesn’t count positions that were assigned as losses. The only way I get a loss according to my tracking is if I close a position with a negative net credit. I took assignment on 3 trades. If those 3 are counted as losses, my win rate comes down to 92%.)

I continue to split my accounts between two strategies. One is to trade mostly credit spreads and naked puts in margin accounts and the other is to sell cash-secured puts & covered calls (i.e. “the wheel” strategy) in non-margin and IRA accounts. As I wrote in my January update of my mortgage pay off, I am starting to do some “poor man’s covered calls” as well. The goal for the margin accounts continues to be to 1) raise cash to increase trading capital and 2) run through my mortgage pay off strategy. The other accounts are reinvesting the profits into stock positions for future growth or passive income via dividend stocks.

Biggest Winner

My favorite part about writing these monthly reviews is looking back at what was my biggest winner and loser. Since I am doing so many trades in a month, each trade is closed and put behind me quickly. It’s only because I keep detailed records of each trade that I can look back and learn what’s working and what isn’t.

My biggest winner for January came from a poor man’s covered call on $AAPL. On January 26th I opened a $100 strike June 2022 Call LEAP contract for $49.50 ($4,950 total). I’m bullish on Apple going higher. This contract gives me almost 18 months to be right and gives me a break-even of $149.50. I then sold a covered call at $152.5 strike for the January 29 expiration for $1.85 per contract ($185 total). Due to the frenzy around earnings (which Apple killed by the way with quarterly revenues topping $100 billion!) the premiums were pretty rich even for such a short dated contract. I closed it two days later (one day before expiration) for a net credit of $178.34. This was all in an IRA, so it’s all mine to keep!

I will continue to sell covered calls at $150 or above to generate income from that LEAP contract and hope I don’t get assigned. If I do, however, I know I will make a profit because my break-even is at $149.50. I may occasionally sell credit spreads if I think there is a chance the stock price could blow past my covered call. Selling a spread is more likely to allow me to roll the position up when I move it out because of the long call as extra “protection” allows me to widen my spread.

You can see my LEAP is in the red at this point. With 16 months remaining in the contract, however, I’m still feeling pretty good about it.

Biggest Loser

I’m going to consider a cash-secured put that I was assigned at expiration on as my biggest loser for January. It was a January 29 short Put on $SBUX at the $99 strike that I sold on January 7th. I collected a $1.25 credit ($124.34 net commissions), but was assigned while the shares were trading at $96.79. Therefore, at assignment, I was down a net $96.66 ($1.2434 – $99 + $96.79). Looking at the chart below you can see I had a comfortable margin of safety until it really dragged down just before expiration.

Fortunately, I happen to think Starbucks is a fantastic business and was not worried at all by the assignment. I immediately sold a covered call that, as you might expect from looking at the rebound at the beginning of February, is now in the money and looking like I will get assigned in the other direction now! This one was also in an IRA so no tax-man to collect on all these trades.

2021 Goals

Another great thing about writing these blogs is that they hold me accountable. In my December review I posted some goals for the year. Here’s a look at how they are going so far:

Contribute $6,000 to my ROTH IRA. CHECK! I already funded my ROTH IRA in the first few days of the new year. Now the trick is to put those dollars to work!

Build $100/month in passive income, primarily from dividends. I want to finish 2021 with a forward looking $100/month in 2022. I am now tracking my dividends separately from my options trading. I collected $55.97 in January. The biggest contributor to that was a quarterly dividend from $SPY.

$10,000 in non-W2 income. It will take $833 per month on average to hit this. Adding the $55.97 from dividends and $751.86 from my taxable accounts puts me at $807.83. Very happy to be at 97% of the monthly goal in January!

Increase our 401k contributions. I have increased my contributions to hit the maximum $19,500 by the end of the year. My wife’s contribution has remained the same so far. We’ll see if we are able to maintain that throughout the whole year, but we are off to a great start.

Increase net worth by 30%. A 30% net worth increase for the year will take a 2.21% compounded monthly return. For the month of January our net worth was up 2.51%. So we’re on track! As I wrote in my post where I set this goal, an increased savings rate, at this point in our accumulation phase of growing our wealth, has a dramatic impact on our net worth. As we grow our net worth we will be more subject to market conditions (assuming we have a decent amount of our wealth in the stock market, for example).

That’s a wrap on January. We are off to a slightly slower start than January so we’ll see if I can close the gap for another record breaking month. If not, no sweat. I’m trying to stay on a consistent path of progress and not looking for home runs.

Disclaimer: I am long $AAPL, $SBUX and $SPY. I am not a financial advisor. This is not investment advice. Please do your own research before investing in anything discussed herein.

Recapping from last month, I had put a total of $220 towards my mortgage principal from options trading profits, saving a total of $338 in interest over the life of the loan. I started to diversify away from putting all my profits straight into my mortgage by beginning to split it three ways: mortgage principal, preferred stock, and Hedgefundie’s Excellent Adventure. With everything included, my $3,328.42 invested in this strategy had returned $470.38 (14.1% ROI/69.7% CAGR!). Surely those returns aren’t sustainable, right?!

In my fourth month, my options trading returns set another record-high of $188, a 5.2% return on capital. My principal barely grew from $3,498.35 to $3,515.08 however, thanks to a big stumble in the markets in the last trading day of January.

For the most part I have continued the same strategies from the past few months. I did add a couple synthetic covered calls (aka “poor man’s covered call” or “PMCC”). I will share those positions and strategy below.

My positions & trades

$AAL, 100 shares at $13.98 average ($1,398 total principal). Principal is currently up 22.8% ($319), however I currently have a $16 covered call position expiring on February 19, limiting my capital gains to $202 total. I closed two positions for the month and for a profit of $34. Similar to last month, I collected a net credit of $12 after rolling up from a $15.50 strike position to the current $16 position.

Last month I mentioned I may continue to sell at the $15.50 strike even if it stays in the money. I opted to roll up to the $16 instead. American Airlines continues to have some very high implied volatility and I think some longterm upside. In the short term I’m really limiting my monthly returns by continuing to roll up, but I think it will pay off over the next few months in terms of total return.

As a sneak peak to February’s update, I’ve actually already rolled up to $17. This time with a very respectable credit due to the reddit frenzy over stocks like $AAL. I also sold another put credit spread at the $14.5/$13.5 strikes.

$APHA, no open stock positions. I continued selling cash-secured puts on Aphria this month for some modest profits. I closed two trades for a combined $23 profit from a maximum collateral of $700, which is a 3.2% return.

In recent days $APHA has really taken off. If I choose to sell more puts I will most likely switch to credit spreads to limit my downside and give me more flexibility with rolling positions down and out when challenged. Currently I have a $13/$12 put credit spread for the February 26th expiration.

$CLSD, no open positions. I sold one cash-secured put on Clearside Biomedical at $2.50 for a credit of $41. I came across this one after reading this “breakout” post over on Seeking Alpha. The article was compelling enough for me to make a speculative trade on it. It worked out, and I closed the trade with a $21 profit a few days later, leaving me with an 8.4% return.

$GE, 1 LEAP January 21, 2022 $5 Strike at a cost of $6.55. GE and MRO (below) are my first attempts at synthetic covered calls (aka “poor man’s covered call” or PMCC). I’ve had good success in the past few months using typical covered calls on stocks like $AAL, $GPRO & $FCEL. Rather than purchasing 100 shares of a stock, I am buying a deep in the money LEAP contract to use as collateral for selling my covered calls. So instead of paying $1,140 for 100 shares of $GE, I bought 1 LEAP contract for $655. When I sold a $12 strike covered call for a $.38 credit, I got a return of 5.8% (38/655) vs. 3.3% (38/1140).

So the obvious benefit is you are putting up (and risking) less capital. There are two main drawbacks to using this method vs. using typical covered calls to consider. The first is that this is a leveraged position. So when $GE goes up by 5%, the price of my LEAP goes up by ~8%, and when it goes down by 5%, I’m losing ~8%. So this drawback actually goes both ways. The other major drawback is my collateral now has an expiration date! This means that if $GE closes below $5 next January, I lose all of my principal. However, I know I will be selling lots of premium before then and feel confident that I will have plenty of opportunities to get out for a profit or sell for a more manageable loss before then.

I am currently selling $12 strike covered calls and look forward to showing those results in the next month.

$GPRO, no open stock positions. In January I had some good results with selling put credit spreads on Go Pro. I closed a total of two trades for a total profit of $39. The largest spread I had for the month was $200, so that’s a 19.5% return. It’s really tough to beat the ROI of credit spreads.

I adjusted one contract by moving the long Put leg down from $7 to $6 strike when the price started challenging the $8 strike. I had decided that I would be OK with taking assignment at $8 if it came to it, so I was willing to increase the spread to $2, increasing my max loss for the trade but not effecting the likelihood of the position getting assigned. In the end the stock moved up dramatically about a week later so I decided to close it when there wasn’t much extrinsic value remaining. I then opened a similar position that same day with an expiration of one week later for a high probability “easy” profit.

$M, no open stock positions. Macy’s is now trading in the mid teens. Crazy that I was selling covered calls in the $6 range when I started. Here is an example of where I could have made a lot more money just buying and holding. But who knew the stock would nearly triple in a few months? For this month I closed 3 positions for a total profit of $32. I ended the month with another credit spread with a potential profit of $20.

$MAC, no open positions. I just had one trade on $MAC for the month for an $8 profit (5.3% return). I found $MAC on a Seeking Alpha comment. Liquidity wasn’t great so I decided to not continue trading it. It looks like it was caught up in some $GME short-squeeze mania at the end of the month that I wasn’t aware of until looking at the chart just now. It has more that 50% short interest, so it was an easy target for the short-squeeze crowd.

$MRO, 1 LEAP January 21, 2022 $5 Strike at a cost of $3.80. As I wrote above regarding $GE, I am going long with a LEAP contract on Marathon Oil Corporation. I think as things begin to open up we will see an increased demand in oil, raising oil price and profits for many of the oil corporations. I closed two trades earlier in the month for a profit of $31. At the end of the month I had a covered call at the $9 strike with a credit of $34, a 9% potential return.

Extra Mortgage Principal Paid

As I explained in last month’s post, I am no longer putting all profits (less taxes) into the mortgage principal. I think I can do better with other fairly passive, and more risky, investing. Those profits, which will beat the 3.125% return that I get by paying down my mortgage, will then go towards the mortgage. My new minimum goal for the mortgage is 1% of the beginning portfolio value each month. January began with a value of $3,498, so I rounded it up to $35. With a combined $255 put towards my mortgage principal in three months, I will save $392 in interest over the life of the loan.

Preferred Stock

My first passive alternative to directly paying off my mortgage principal is preferred stock. At the end of January, my preferred stock portfolio for this mortgage pay off strategy was worth $116.97 and consisted of five different positions. I purchased three preferred stocks for the month, totaling $69.27. I do plan to write a bit more about my strategy with these, but for now, here are my current holdings (1 share of each):

SCE-J, 5.375% coupon with a yield on cost of 5.55%

I haven’t received any dividends on these positions yet, but they will go toward the mortgage when they come in. I hope to buy at least one new preferred stock each month.

Hedgefundie’s Excellent Adventure

This strategy is purely for capital growth. The target allocation is 55% UPRO/45% TMF, which are both 3x leveraged ETFs. Once their value is enough to reduce my mortgage term by one month, I will put it all towards the mortgage and start over. I have yet to rebalance this because the total value is still so small, but rebalancing is critical to this strategy’s success. For January, $13 was put into $UPRO and $12 into TMF. At the end of the month, the value in these funds was $60.51. To reduce my mortgage by one month I would need to make a $610 payment, so still a long way to grow.

Accounts Summary

Of the $188 earned from options trading in January, $58 was set aside into the ULP for taxes, $35 was put towards the mortgage principal, $69.27 was invested into preferred stocks and $25 was invested into Hedgefundie’s Excellent Adventure. The remaining $.73 will stay in my trading account. The trading account’s value ended January at $3,515.08, preferred stock was at $116.97 (with a forward yield of 7.4%) and Hedgefundie was at $60.51.

Benchmark Comparisons

In my introduction post I identified three different benchmarks I will be comparing my performance to. Benchmark #1 is putting all of my savings from my refinance, plus a 1 month skipped mortgage payment, into a savings account. When I wrote that post I was actually getting 0.6% APY, but it has reduced twice down to 0.3%. Benchmark #2 is putting all of those savings straight into extra monthly payments to the mortgage principal. Finally, Benchmark #3 is simply buying $SPY.

After 4 months I have invested $3,492.63 (initial $3,000 + $164.21 per month). Benchmark #1 is at $3,497.02, Benchmark #2 is at $3,517.41, Benchmark #3 is at $3,643.84. My actual total has just passed the $4k mark at $4,005.76. This is a total return of $513.12, or 14.7% (50.9% CAGR). My returns include the value of my principal in my trading account + the monthly contribution of $64.21 and interest into my savings + the difference between the original loan and what is actually remaining this month. My results are beating Benchmark #1 by 14.6%, #2 by 13.9% and #3 by 8.6%.

Obviously I am very pleased with the results so far and can only hope things continue to grow at a similar rate. What’s especially cool about all of this is that it all came from refinancing my home loan. The 3.125% rate I ended up with is pretty mediocre relative to what the averages are at right now, but because it allowed us to skip 1 month of mortgage payments and allows us to save $164.21, and because I am aggressively investing it rather than sticking it in a “high yield” savings account or, worse, spending it, I am slowly turning that opportunity into wealth.

Disclaimer: I am long $AAL, $MRO, $GE, $CDR-C, $NRZ-A, $NRZ-B, $PMT-B, $SCE-J, $SPY, $UPRO and $TMF. I am not a financial advisor. This is not investment advice. Please do your own research before investing in anything discussed herein.

The market had another strong month, though not quite as great as November. $SPY was up 3.3% in December, closing on New Year’s Eve at an all-time high. If I had told you there would be a worldwide pandemic and most of the world would shut its doors in 2020, I bet you wouldn’t have guessed the S8P 500 would be up more than 16% by the end of year? Crazy.

Since I’m just a few months into this blog, it doesn’t make sense to have a big yearly review of my performance in my accounts. I will review some changes I made this year, what I plan to do going forward, and some goals. But first, let’s wrap up December!

For the month of December, my total profits from options trading were $2,320.73, my best month yet and nearly 10% more than last month. That’s a total portfolio return of 2.1% and below the market’s 3.3% for the month. However, my total portfolio value across all accounts – which includes options trading profits, current stock & options positions, contributions & withdrawals for extra mortgage principal payments – was up 3.6%, just edging out the markets performance. The portfolios had net contributions of $246.30 for the month. I closed 69 options trades with a win rate of 97%*.

(* That win rate is a bit misleading because it doesn’t count positions that were assigned as losses. The only way I get a loss according to my tracking is if I close a position with a negative net credit. I took assignment on 5 trades. If those 5 are counted as losses, my win rate comes down to 90%.)

I continue to split my accounts between two strategies. One is to trade mostly credit spreads and naked puts in margin accounts and the other is to sell cash-secured puts & covered calls (i.e. “the wheel” strategy) in non-margin and IRA accounts. The goal for the margin accounts continues to be to 1) raise cash to increase trading capital and 2) run through my mortgage pay off strategy. The other accounts are reinvesting the profits into stock positions for future growth or passive income via dividend stocks.

Biggest Winner

My biggest win of the month, and ever by total profit, was a cash-secured put on $LOW. Lowe’s has shown to be very resilient during the COVID shutdowns thanks to many people taking up home improvement projects (myself included! In fact, I swiped my Lowe’s credit card countless times in 2020). There was a big pullback on November 9 and I decided to open the December 18 cash-secured put at the $150 strike for a credit of $3.75. At one point I was in the money, but held my ground and let it ride, knowing that if I was assigned I would be happy to own $LOW at $150. About a week before expiration the stock jumped back up and I took that as an opportunity to close the trade for a net credit of $340.68, a 2.3% return (25.1% annualized).

Biggest Loser

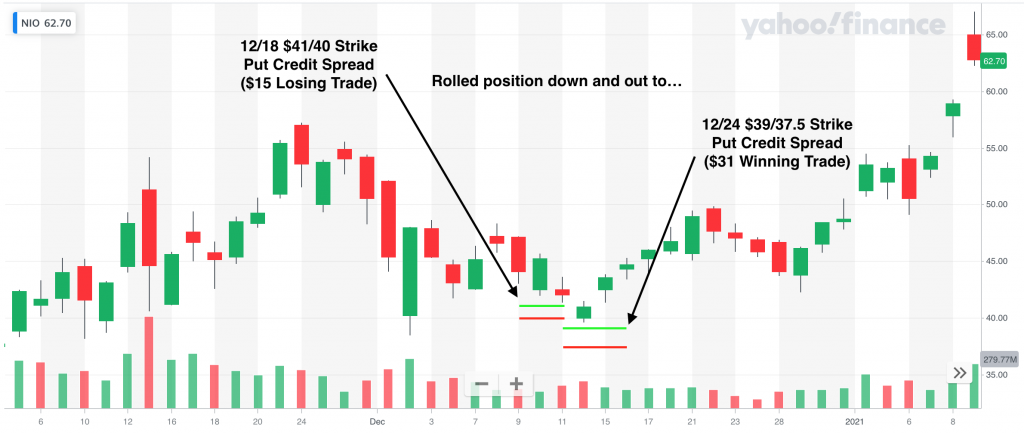

My biggest loss was on Chinese EV company $NIO. The loss was only $15, and looking at the chart below, would have been a winner if I had held until expiration. It was a Put credit spread for December 18 expiration at the $41/$40 strike. I opened the trade on December 9. The stock started moving against me, and rather than holding the line, I decided to roll out one week and down a bit. I also increased the width of the credit spread, allowing me to bring in some credit for this trade. I ended up with the December 24 expiration now at the $39/37.5. Once the stock began moving in my direction, I decided to let it go and pocket a $31 profit. So net was a positive $16. Not bad for my biggest loser!

I had an actual paper loss due to an assignment on $PFE at expiration. I had a cash-secured put at the $41 strike. At expiration, $PFE was trading at $37.68, so the paper loss was $332 ($41-37.68). I did collect $102 in credit, so net is a loss of $230. Pfizer is obviously a very strong company and am not worried holding a long position. I will sell covered calls at above $41 and collect premiums until I get assigned. Currently I have the February 19 expiration $42 covered call for a net credit of $64. If I hold it until expiration, that is a 9.2% annualized return. In addition, Pfizer currently pays a dividend of ~4%, which I will collect until the shares are called away.

Looking forward to 2021

In my first few months of options trading I’ve had some really great success. While I’m not about to retire from my day job and go YOLO on selling options, I do see potential to make this sort of a side hustle. One thing I am realizing, and one of the things I am drawn to, is it is not at all a passive form of investing — at least not the way I’m doing it! I do, however, believe that passive index investing is a great strategy for building wealth and that is what my wife and I are doing in our 401k’s.

With that said, here are some of my investing related goals for 2021 (in no particular order):

Contribute $6,000 to my ROTH IRA. I opened my ROTH towards the end of 2020. With $12,000 in the account I should have some good options for… options trading.

$10,000 in non-W2 income. This includes profits from options trading, dividends, interest, etc. only in my taxable accounts. This is pretty aggressive, and definitely a stretch goal. Last month was my best month of option trading profits yet at $620 for the month in those accounts. I will need to average $833 per month.

Build $100/month in passive income, primarily from dividends. Again, this is in my taxable accounts. The goal isn’t to have $1,200 in dividend income for the year as I think that is too aggressive for me at this point, but to be averaging $100/month as I go into 2022 (or $300/quarter since most stocks pay out quarterly). I haven’t added up all the numbers, but I was probably around $60/month in 2020. I might start including dividend income in my monthly updates.

Increase our 401k contributions. We certainly won’t be in a position to max out both of our 401k’s this year, but I’d like to get there over the next few years.

Increase net worth by 30%. This one is also a bit of a stretch goal. As we become more invested each year, net worth increases will become more subject to market conditions and less due to our savings. We benefited from being able to put more into the market in March and April of last year, and it’s unlikely we will have another opportunity like that. But who knows! We ended 2020 up 32%.

Reduce mortgage length by 1 month. As a part of my mortgage pay off strategy, I’m hoping to be able to pay enough towards the principal to reduce the length of my loan by one month. As of this month, I need to put another $643 towards principal to accomplish this. At my current rate of monthly progress, that would take less than 6 months to achieve. However, I’m not putting quite as much directly towards the mortgage as I did the first two months. In the long run it will “pay off”, but may make this goal more difficult to achieve in 2020.

First off, HAPPY NEW YEAR! This is not a yearly recap post and since I just started this blog a couple months ago, I’m not sure I will be making one. I will likely have a forward looking 2021 post though. Now, onto the post…

After two months of this experiment, I had put a total of $187 towards my mortgage principal from options trading profits which will equal $288 of interest saved over the course of my 30-year 3.125% loan. In addition, my options trading account principal of $3,200 (which was/is funded from savings from refinancing) was up to $3,240.86. A great start and already ahead of my initial goal by 2.6%.

I have continued to outperform in December, my third month, with $170 in options trading profits which is a 5.1% return on capital! In addition, my principal has grown to $3,498.35, 6% more than the $3,300 added to the account thus far. Remember, that 6% is after deducting taxes and withdrawals from the account to make the extra mortgage principal payments.

This month I have made a dramatic tweak to how I am divvying up my options trading profits towards my extra mortgage principal payments. More on that after I review this month’s positions and trades.

My positions & trades

$AAL, 100 shares at $13.98 average ($1,398 total principal). Principal is currently up 15.4% ($215.08), however I currently have a $15.50 covered call position expiring on January 29, limiting my capital gains to $152 total. I closed two positions for the month and for a profit of $74. I collected a net credit of $12 after rolling up from a $15 strike position to the current $15.50 position.

Going forward I will most likely continue to sell the $15.50 strike even if it stays in the money. I should be able to collect a large credit at least one more time. I will consider moving up to the $16 strike if I can still collect a decent credit. My main objective here with this account is to generate income, with a secondary goal of capital preservation and tertiary is capital growth, however I don’t want to leave easy money on the table in the name of current income. Like so many things in life, it is a balance.

$FCEL, no open positions. This month I finally had my shares of FuelCell Energy called away. In the end, I made about 30% in profits from that position. BUT I missed out on a $1,000 profit! This was a classic case of picking up pennies in front of a steamroller. In my defense, the pennies were very shiny and no one could have seen that steamroller coming!

I only closed that final $2.50 covered call for a $10 profit. On to the next one!

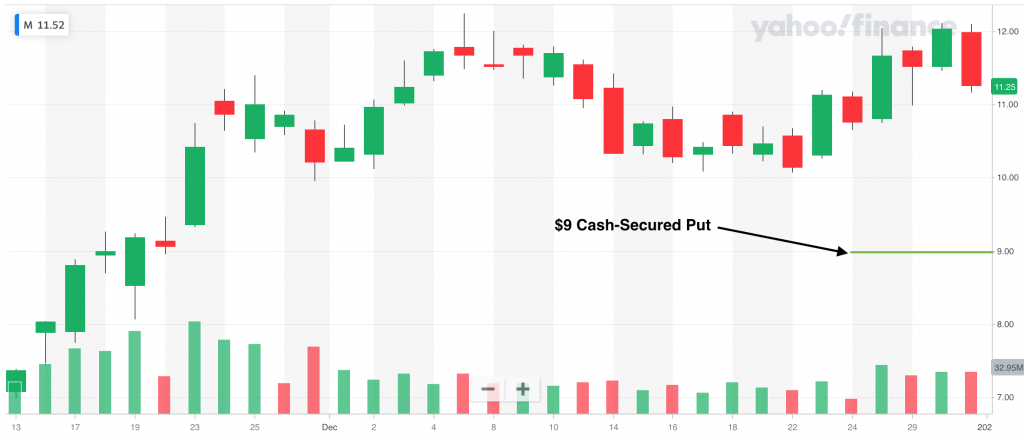

$M, no open stock position. Last month I had my Macy’s position called away at $6.50. I had just about given up on the stock when I saw an easy trade by selling a $9 Put for January 15 for a credit of $15. This trade is a 1.7% return (26% annualized), so it meets my 1% goal.

If the stock drops suddenly to below $9 and I am assigned, I expect the premiums to go up and good potential for selling covered calls.

$GPRO, no open stock position. Similar to Macy’s, Go Pro was a stock that was called away from me in November. I decided to sell some puts this month, and that worked out well for me. I closed three positions for $34 profit. My highest strike price on those positions was $7.50, so that $34 was made using $750 as collateral, which is a 4.5% return.

I currently have a put credit spread at the $8/$7 strikes that I collected a credit of $27. In the past couple months I have had a lot more success with simply selling naked positions (cash-secured puts or covered calls, technically) than with credit spreads. However, more recently I’ve found some decent success with credit spreads as long as I’m willing to roll it out when I’m challenged. Contrary to a lot of advice, I am generally able to do this while collecting a credit if I widen the spread. So if I start with a $1 spread, I roll it out and down (for a Put) or up (for a Call). I’m therefore increasing my potential loss, which is why it generally isn’t advised, but it’s working for me right now so I’m going to go with it.

$APHA, no open stock position. I continued selling cash-secured puts on Aphria this month for some decent profits. I’ve thus far avoided getting assigned the stock. I closed three positions for a total profit of $33. Similar to the $GPRO puts, those $33 were earned with a maximum collateral used of $700, so a 4.7% return.

I currently have a $6.50 cash-secured put for January 15 open that I am watching closely. I collected a net credit of $18 after rolling down and out from December 31 $7 strike. That’s looking like a pretty smart move since it closed at $6.92 on New Year’s Eve and I would have been assigned. I may look to roll down and out to the $6 strike if I am able to for at least a 1% credit (i.e. $6).

$MRO, no open position. I had one trade on Marathon Oil Corporation this month, a credit spread from $5.50 to $4.50, with a profit of $9.

$MAC, no open stock position. I have an open credit spread on The Macerich Company (a REIT) from $9 to $7.50. I collected a credit of $13.

Extra Mortgage Principal Paid

As I said earlier in the post, I’ve changed how much of my profits I am putting straight into my mortgage principal. Perhaps this deserves its own lengthy post, but essentially I am wrestling with the opportunity cost of locking those profits up into the equity in my home. Now don’t read this as my giving up three months in.

As I listen to more finance podcasts and Youtube videos, I often hear about the velocity of money. When money is moving, it has velocity. Option trading is great because you are constantly moving money from one opportunity to the next. The money has velocity. When a dollar goes into my mortgage principal, it comes to a screeching 3.125%-halt. Remember my goal, which I am currently outperforming considerably, is 1% a month or 12% a year! Wouldn’t it be great if I could keep the velocity going before slowing it way down with my mortgage?

Of course it would be. However, the only reason anyone ever put extra principal into a mortgage was for that guaranteed rate of return. It’s essentially risk free! Compare that to a 0.4% APY “high yield” savings account and that 3.125% rate now looks pretty good! Based on my performance in the past three months, I should sell options with every dollar I have since my returns are so great, right?! Well, no. I’m not so naive to think that this will continue on forever without any losses.

All this to say that I will continue to remove my profits from my mortgage payoff trading account. I will continue to set aside the correct amount for taxes. Assuming I am left with more than my 1% goal for the month, I will take that 1% and put it towards my principal. The remaining balance is where I plan to… diversify.

Preferred Stock

I’m not going to take the time to explain the nuances of preferred stock here (Investopedia definition). It is often referred to as a hybrid of stocks and bonds. Anyway, I have been reading a book called Preferred Stock Investing and I believe there are some great opportunities for some fairly high yields. This month I actually bought two preferred stocks with dividends that yield an average of about 8%. I plan to take those dividends and put that money into the mortgage principal. Instead of taking my super high return from options trading and slowing it down immediately into my mortgage, these dollars will keep speed for a while longer.

While I expect (hope) to outperform even these high yields of 8% with my options trading, these income source has the benefit of being nearly completely passive. Options trading is one of the most active forms of trading, I am learning. Diversifying profits away from the options trading and into more passive income streams will help keep everything more sustainable as the account size grows.

Hedgefundie’s Excellent Adventure

Honestly, not really sure where to start with this. Think leverage. Think risk parity. That’s Hedgefundie’s Excellent Adventure. The strategy, specifically, is 55% in a 3X leveraged S&P 500 ETF $UPRO and 45% in a 3X leveraged long term bond ETF $TMF. Rebalance as required. There’s a great write up of the strategy here (it initially started from an epic thread on the “Bogleheads” forum).

After setting aside my portion straight towards the mortgage and purchasing any preferred stocks for the month, I will split my profits 55/45% into the Hedgefundie strategy. For now, my plan is to let this pile grow until I reach enough to reduce my mortgage term by one month. As of now, I need $643. This allows me to benefit from the great growth potential of leveraged ETFs while minimizing the risk since I won’t be letting it grow indefinitely.

So how did I slice this complicated pie this month?

After taxes ($53 into ULP), the $170 profits was $117 net. Instead of putting that $117 total into the mortgage as I would have in the previous two months, I put just $33, which is ~1% of my account’s starting principal of $3,240.86 for December. I bought two preferred stocks ($NRZ.A for $23.22 and $PMT.B for $24.75) for $48.15. Finally, I invested $36 into the Hedgefundie strategy, as $20 in $UPRO and $16 in $TMF.

With a combined $220 put towards my mortgage principal in three months, I will save $338 in interest over the life of the loan. In addition, my preferred stocks are now worth $49.55, a 4.2% return, and will yield ~8% going forward ($3.88 in dividends annually). Finally, the Hedgefundie’s Excellent Adventure is also up 4.2% to $37.53.

Benchmark Comparisons

In my introduction post I identified three different benchmarks I will be comparing my performance to. Benchmark #1 is putting all of my savings from my refinance, plus a 1 month skipped mortgage payment, into a savings account. When I wrote that post I was actually getting 0.6% APY, but it has reduced to 0.4%. Benchmark #2 is putting all of those savings straight into extra monthly payments to the mortgage principal. Finally, Benchmark #3 is simply buying $SPY.

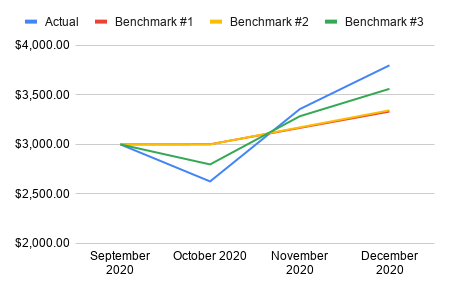

I continued to make gains across all three benchmarks this month. When considering the value of my principal in my trading account + the monthly contribution of $64.21 and interest into my savings + the difference between the original loan and what is actually remaining this month, my total value is at $3,799 after the month of December, a 13.2% improvement over November. That beats Benchmark #1 (all savings) of $3,332 by 14.0%, Benchmark #2 (extra mortgage payments only) of $3,344 by 13.6% and Benchmark #3 ($SPY) of $3,561 by 6.7%. Below is a chart of my progress so far.

Thanks again for following along. Looking forward to more progress in 2021!

Disclaimer: I am long $AAL, $UPRO and $TMF.I am not a financial advisor. This is not investment advice. Please do your own research before investing in anything discussed herein. This post contains affiliate links.