Rather than listing out every trade I made last week, going forward I am most likely going to highlight a couple trades only. Like my options trading skill level at this point, this is all still a work-in-progress and hope to settle into a posting routine that is regular, sustainable and still achieves a level of transparency.

First, the basic numbers: Closed 18 trades for $23.63 profit (78% win rate). Opened 17 trades.

This week I plan to highlight two of my biggest losers to date: a trade in Nike and Tesla. One of which I would probably make again, the other I hopefully have learned something from and won’t make the same mistake in the future.

I opened this trade the day before earnings were to be announced. I made a guess that, due to COVID-19, the earnings report would not merit the recent rise in the stock. I guessed wrong, as Nike’s online presence appears to be taking off. In addition to the stock price immediately blowing past both my short and long strike prices, implied volatility had increased as well. So not only did I pick the wrong direction of the move, I also was on the wrong side of volatility. On top of all this, the liquidity in NKE options trading isn’t all that great. If I was set on making a trade, I should have either waited until after the earnings to see what happens, or I really wanted to make a speculative play, buy either a long put or call so that I still have defined risk and I don’t lose to the increased volatility, as well. I’m curious how a basic calendar spread would have done here.

This one is my biggest loser to date. It is my first time trading a spread with more than a $1 spread, with this one being $2. I took in a decent premium thanks to the high implied volatility, limiting my possible loss to $125. One thing I also was able to do was sell some put spreads below the market, effectively making an iron condor. I rolled those up a bit as I approached expiration, picking up a credit each time to help decrease my total loss. Tesla goes all over the place, often for no apparent reason, which is why we see such high premiums in the option contracts. For that reason, I will chalk this one up as just a loser and nothing more, rather than a bad trade like the Nike one above.

My biggest winner from the week? Not surprisingly: TSLA. I made $25 on a Put credit spread at $388/387 with the same expiration as the previously mentioned Call credit spread. I was actually able to roll this one up closer to the money for an extra $6, putting me at $31 on the put side for TSLA. Not enough to cancel out my loser, but certainly is better than just taking the full $125 loss I would have had if I didn’t react at all.

Earlier this year I left my job to take a similar role at a company with a better location and hopefully a bit more upside growth potential (and a little bit more money, of course!). In just over four years there, my 401k had grown to nearly $40,000. I let it sit there for the past six months while I considered how I wanted to proceed. Once the COVID-19 induced pullback happened shortly after I left, I was reluctant to move it since I would have to close all my positions at a big loss. The account balance dropped down to about $31,000, which was actually a negative overall invested return at that point (i.e. I had contributed more to the 401k than it was currently worth)! I felt the market would recover most of its losses fairly quickly (I was right… and am happy I invested extra cash in our taxable brokerage accounts during that time) and was concerned some of that recovery would happen while I moved funds around. So there it sat for about 6 months.

I considered rolling it into my current employer’s 401k plan so I could keep it all together. The other benefit to doing this is that I would have a larger amount in my 401k to take a loan out against in case I found the right deal I wanted to pull the trigger on and needed some extra resources (I know most of the literature out there says 401k loans are a bad idea, but I’m not considering it to buy a truck or an RV! This would be exclusively for buying assets like rental properties.).

One thing I don’t like about the 401k’s is that I don’t have that many options to invest my money. With an IRA, I can pick and choose my investments. And in the event I get tired of picking and choosing, or I’m unhappy with my performance, I can always just put my money in some ETF’s or just buy the same mutual funds I used to have in my previous 401k.

As I started to see the power in options trading for increasing portfolio returns, I began to lean much more favorably toward an IRA. I considered rolling it over into a Roth, but my household income is still below the maximum income limit to contribute to a Roth, so I still have the option to fund a Roth going forward without paying a large tax bill now for the rollover. If I ultimately open up the Roth, I will definitely discuss my strategies for that account as well. For now, it’s just another traditional IRA. A final point that I think is worth pointing out is that my wife and I still have 401ks that we contribute to regularly, which gives me more freedom to invest this portion myself.

How I am investing ~$42,000

After the bounce back from the COVID-19 panic, my portfolio climbed back, and eventually comfortably surpassing its previous highs, to almost $42,000. This past Friday morning I opened my account and to my delight found the wire transfer was complete! So much cash! So many possibilities. Without going into too many gory details on how I plan to trade this account, here are the trades I made in day 1:

I bought SPY, QQQ and IWM. These are my reference point. I think it will be fun to always check these holdings to get an idea of where I would be if I had just invested all my cash into one of these (or all three) index funds. The bar has been set!

I sold a put on AAPL. As long as I’ve know what a cash-secured put was I wanted to “write a put” on Apple! Finally I have the resources to do so. I sold the November 20 $106.25 put for a $170 credit. I immediately bought one share of Apple at $120.31.

I sold a put on O. REITS are on my wish list for this account, including O first and foremost. I sold the November 20 $60 put for a $128 credit. I then bought 2 shares of Realty Income at $60.56.

I sold a put on SBUX. Starbucks and Apple. A match made in heaven. I sold the October 30 $85 put for a credit of $100. I then bought one share of Starbucks at $88.70.

I sold a put on T. I sold the November 6 $26.50 put for $45 and then, you guessed it!, bought one share of AT&T at $27.46.

I now have two-thirds of my opening balance put to work, with $1,1512 in long stock, $28,677 being held as collateral, and an extra $75 in cash generated. Things are off to a fine start!

$1 Million Portfolio

Here’s my pie in the sky: turn ~$42,000 into $1 million by the time I retire (which we will say will be 30 years from now). Since my wife and I both have 401k’s, we won’t be able to contribute to this account going forward, which means I will have to do all the heavy lifting myself. In order to do this, I need to achieve a CAGR of 11.2% (or 0.89% compounded monthly). A lofty goal indeed. Let’s see what happens!

In my last post on this strategy, I introduced the plan to pay off my recently refinanced mortgage early with returns generated from options trading. The pros and cons of paying off a mortgage early aren’t discussed in that post or here, but I will likely write something about it in future posts. The capital used to fund this trading is the amount we are saving due to refinancing our loan at a lower interest rate, which is $164.21 in monthly savings. We were able to skip one month of mortgage payments (we closed in September and our first mortgage payment on the new loan isn’t due until November). Our skipped payment is the initial trading account’s starting balance (“principal”), which is $3,000. $100 of the savings will be added to the principal each month, with the remaining $64.21 going into our savings account (which yields 0.6%), at least for now.

There are further details in that introduction post, including three different benchmarks I will be comparing my results to.

In this post I want to dig a little bit deeper into the strategy I plan to use to generate my monthly return goal of 1%. The basic concept is to sell cash-secured puts and covered calls. If you are new to options trading, here are two good resources to explain what cash-secured puts (here’s a good explanation and Option Alpha has a good video) and covered calls (Investopedia and Option Alpha video) are. Basically, selling a cash-secured put gives you a premium up front for your obligation to purchase the shares at the chosen strike price. It is cash-secured because the amount you are obligated to purchase the shares at is used as collateral and is not available for trading until the contract is closed. Selling covered calls gives you a premium up front for your obligation to sell shares you currently own at the chosen strike price.

It’s actually very easy to generate 1% return on your principal each month using either of these strategies. The trick is to preserve that principal throughout market cycles. Let’s go over the risk of each strategy and how I might lose money doing this strategy. First, if I sell one $9 put contract on a stock currently trading at $10, and it drops below $9, say $8.50, then I will be down $.50 per share (or $50 total since one contract is equivalent to 100 shares). Remember I collected a premium up front for selling the put, so I’m actually down $50 less the premium received. If the premium was more than $50, I would actually still be profitable at $8.50 per share. As you can see, though, if the stock crashes, I’m losing money. If it stays above $9 at expiration then I keep the entire premium and don’t acquire the shares.

Now let’s say that I already owned the shares at $10 per share. I sell a covered call at a strike price of $11. If the stock goes above $11, I’m forced to sell it at $11 per share, even if it took off to $15. You lose the upside potential by selling covered calls. If it drops to $8.50 like the previous scenario, then I am now down $1.50 per share minus the premium received. In that situation, I still own the shares so I can sell a covered call at $11 (or $10.50 or $10 or…) the next month.

In an ideal world, I will sell puts, and the stock will always stay above my strike price. I keep the cash in my account and keep collecting premiums. If I get assigned, again ideally I just sell covered calls at above my average price on the stock. As soon as the stock comes back up to my strike price, I sell it for a profit and get to keep the premium. This is known in options trading as the wheel (Medium article).

The premium received on puts diminishes the lower the strike price is, and it diminishes on calls the higher the strike price is, relative to the stock’s current price. So if I get assigned a stock that I sold a put on, and it absolutely tanks, I won’t be able to sell calls at a profitable price because the premium will be so small. This is really the worst case scenario.

A couple strategies I have to help limit my principal losses:

Diversify the stocks I’m working with. I’m limited by the share price of the contracts I’m selling puts on by the size of my principal since these are cash-secured puts. Starting with $3,000, the most expensive stock I can work with is $30 per share ($30 * 100 = $3,000). If that one stock crashes while I have a contract on it or own the shares, then I could be in trouble. If I instead am using three different $10 stocks, the chances of all three crashing at once is much less likely. Especially if they are in different sectors. Or even better if they have uncorrelated or opposing Betas (Investopedia Beta definition).

Sell puts at a price where I don’t have a high likelihood of getting assigned. This is about not being too greedy or speculative. If my goal is 1% per month, I don’t need to try to get a return of 10% with a very aggressively priced put.

Sell calls close to the money or even in the money. Opposite from puts, if I sell my calls at an aggressive price, I am more likely for the shares to be taken away from me and I lock in my profits. What I’m losing here is the upside of the stock taking off. But my goal of this strategy isn’t growth. It’s to generate regular income to pay down debt while preserving my capital.

Use premiums to lower my average share price rather than withdrawing from the account to pay down the mortgage. If I’m down on a position, I may use the premium I used from selling a covered call to buy shares at a lower price to lower my cost basis. If it lowers my costs enough, this will actually allow me to sell calls at lower strike prices and still remain profitable. 1% in income is my goal, but not at the sacrifice of my principal. Currently, I am thinking I may do this if a stock I own is trading at a price that is more than 5% lower than my cost-basis (Investopedia Cost-Basis definition) and is one strike price lower than my cost-basis (so if I bought the stock at $10.55 and it is now trading at $10.10, I could buy more shares at $10.10, bringing my average down below $10.50 and allowing me to sell a call at $10.50 because that is now above my total cost-basis).

In extreme cases it may be necessary to either sell the shares at a loss or start selling calls at below a profitable level. Hopefully this doesn’t happen, but it’s better then letting my principal go to $0!

Picking Stocks

The fun part! One of the keys to this strategy is to pick the right stocks. It’s best to trade companies that have a solid foundation and are likely to be around for a while. This isn’t a buy & hold strategy, however, so I don’t need to be forecasting 10 years in the future. It’s great if the stock goes up in price, and I can still make money on stocks that drop a little bit. The three killers to avoid are stocks crashing, super low options trading volume, and a large drop in implied volatility, all while holding a position in the stock.

I don’t have a strict set of criteria for stock picking for this strategy yet, but I intend to share my trades each month along with my progress. In time, I expect themes to present themselves and will hone my strategy more and more.

Progress

As long as I am continuing with this strategy, I intend to post regular updates on my progress, including trades made, profits, and the mortgage pay down progress. I am making a separate page here that will show some tables and graphs to keep track of everything in one place.

This plan is already in motion and I have made 7 trades in 4 different stocks so far. I’m excited to share my progress and begin reducing my family’s debt!

I picked this one up after looking over Option Alpha’s stock scanner. I was literally my first couple days into options trading (funny how long ago just a couple weeks ago seems now…) and was trying to get my Level 3 options trading approval through Robinhood. I read online that once you’ve done ~10 trades you are more likely to be approved for Level 3. Since I was still Level 2 when I placed this trade, I couldn’t actually submit this as a single spread order. First I sold, essentially, a cash-secured put (at $19) and, once that was filled, immediately bought the $1 spread (at $18) to limit my risk. I was left with just a $6 credit on an ~80% probability trade… not a good risk/reward situation! Decided to finally close this to take that $94 risk off the table.

SPY Put Credit Spread (October 5, 2020 $335/334 @ +$.28)

From last week’s opening trade: This is my second attempt at reducing a potential loss by selling the opposite trade, effectively making an iron condor. Option Alpha recommends this rather than cutting losses by selling the initial, losing trade (in this case the $341/342 Calls that ended up being profitable thanks again to the dip from the president’s COVID-19 results). In the end, this one worked out for me because SPY opened up on Monday morning. Had I let this expire at the end of the day, I would have kept the entire $28 premium, but since I was basically 50/50 at that point whether I’d make $28 or lose $72, it made sense to close for just the $4 gain.

F Cash-Secured Put (October 16, 2020 $6 @ +$.08)

Max Profit: $8

Collateral: $600

Max Loss: $592

Opened: September 16, 2020

Closed: October 16, 2020

P/L: +$5.33 (After commissions)

Return on Capital: .9% (15.4% annualized)

I am long F in this account with 200+ shares with a cost-basis of ~$8.80. Prior to learning about options, I’ve been lowering that cost-basis by slowly buying more shares. Going to be using cash-secured puts (and covered calls) to hopefully turn this one into a winner going forward.

As mentioned last week, I have held a long position in AAL since it tanked due to the COVID-19 pandemic. I have a comfortable feel for the stock’s recent range now and I will continue to sell calls and puts when the premiums make sense. This trade was triggered when the position fell into my 50% profit target range when President Trump tweeted that congress needs to sideline stimulus package talks until after his Supreme Court nominee is confirmed. Thanks for the volatility, Donald!

ANF Put Credit Spread (November 20, 2020 $13/12 @ +$.35)

TL;DR: My wife was right! From last week’s opening trade: This might sound crazy, but my wife says she has seen lots of “influencers” on social media sporting Abercrombie lately. She thinks it’s going to be a “cool” brand again. I took a look at the premiums available, and they make sense from a risk-reward-probability perspective, so I pulled the trigger. That’s one of the things I love about options trading is that for a small amount of capital, you can make speculative trades that are still high probability of success regardless of whether the stock moves much at all AND have defined risk.

GPRO Cash-Secured Put (October 9, 2020 $5 @ +$.50)

Max Profit: $50

Collateral: $500

Max Loss: $450

Opened: October 1, 2020

Closed: October 6, 2020

P/L: +$26.68 (after commissions)

Return on Capital: 5.3% (325% annualized)

From last week’s opening trade: After successfully closing last week’s short put on GPRO, decided to do another one. If I get assigned, I will sell calls at probably $5. If I don’t, I will probably buy a few shares of GPRO essentially “for free.” Stock took off, so pocketed ~1/2 the premium and bought a few more shares.

GE Put Credit Spread* (October 9, 2020 $6.5/6 @ +$.05)

Max Profit: $5*

Collateral: $650

Max Loss: $50

Opened: September 18, 2020

Closed: October 9, 2020

P/L: +$17.99 (after commissions)

Return on Capital: 2.8% (46% annualized)

This trade was my first attempt at a credit spread, but I wasn’t approved for spreads by my broker yet! So I made my own by selling the $6.50 put and buying the $6 put. GE was struggling around $6.20 for most of the time I had these contracts, but decided I’d be OK getting assigned on this one so I sold my long put for $14, which is the majority of the profit from this trade. GE jumped up the last few days before expiration as well.

Weekly Roundtrip Trades (Positions opened and closed within the week)

I had no roundtrip trades this week. This is because I currently have many at a paper-loss, and those that are winners, are generally balancing out my losers (e.g. losing on a bearish call credit spread, but winning on a bullish put credit spread). I have

This is part of an ongoing strategy I am working on that, in my notes at least, I’m referring to as “ETF Challenger” (it’s a working title, OK!). There are several other trades below that are all part of this strategy, so I’m not going to comment on each one. As my experience grows and I refine the strategy, I will more formally document it, but the idea is to challenge the market when it makes a large move up or down, which is about 1%. I then sell puts or calls at the ~.30 delta, if the premium is high enough. I think I got a little carried away with this in this week, but I chalk it up to learning!

UNM Cash-Secured Put (November 20, 2020 20 @ +$2.30)

Max Profit: $230

Collateral: $2000

Max Loss: $1,770

Opened: October 5, 2020

This is an IRA trade on a stock I’m very interested in going long on. I don’t intend to keep a full 100 shares, assuming I get assigned, but will put some of the premium I earn into buying the shares and then use covered calls to get my initial $2,000 principal back.

I’m starting to warm up to the idea of more cash-secured puts (and covered calls). As I said last week, I’m already long Ford at an average price of $8.80ish. At $7 I’d be willing to add to the position. Will immediately be selling covered calls on this if it gets filled.

GPRO Cash-Secured Put (October 16, 2020 $5 @ +.18)

Max Profit: $18

Collateral: $500

Max Loss: $482

Opened: October 6, 2020

Go Pro has been super hot this week, so premiums are pretty good. The stock is now trading in the $6, so very unlikely this will be challenged again at $5. Will probably let it go until expiration next week.

SLV Put Credit Spread (November 6, 2020 $20.5/20 @ +$.14)

Max Profit: $14

Collateral: $50

Max Loss: $36

Opened: October 6, 2020

This one fits in with my “ETF Challenger” plan. Tuesday afternoon had lots of stocks taking a big dip after the previously mentioned Trump tweet. I tried to jump on the opportunity and put out lots of trades, but had trouble getting fills. This is one that did.

UNG Put Credit Spread (November 6, 2020 $10/9 @ +$.25)

Max Profit: $25

Collateral: $25

Max Loss: $25

Opened: October 6, 2020

See SLV above

SLV Put Credit Spread (November 6, 2020 $20.5/19.5 @ +$.27)

Max Profit: $27

Collateral: $100

Max Loss: $73

Opened: October 6, 2020

Same trade as SLV above, but in a different account with a slightly larger spread.

The market opened big on Wednesday after Trump essentially said, “JK.” As a result, lots of opportunities for “ETF Challenger.” Probably ended up with too many of essentially the exact same position (bearish on the overall market), which will mean either some big wins or big losses. Still learning here, so going to see how it plays out for now.

This trade actually gives me an iron condor on the November 20 expiration with a nice wide range from $9 to $15. Assuming AAL stays within this range, I will probably try to close both positions with one order for a combined ~50% of max profit.

DIA Call Credit Spread (November 13, 2020 $293/294 @ +$.33)

“ETF Challenger”, as above. Actually identical to one of the above trades, but in a different trading account that was able to get filled at a really good premium of $.38.

BAC Cash-Secured Put (October 16, 2020 $25 @ +$.60)

Max Profit: $60

Collateral: $2,500

Max Loss: $2,440.67

Opened: October 8, 2020

I’m looking to get some financial exposure in our IRA account (it’s currently pretty tech heavy), and Bank of America is a stock I’d like to own at $25. Will probably accumulate shares with premiums, and if I get assigned, sell covered calls because I’m not sure we want $2,500 of that portfolio tied up in one stock (unless that money is being put to work with covered calls!).

SKT Cash-Secured Put (November 20, 2020 $6 @ +$.32)

Max Profit: $31.33

Collateral: $600

Max Loss: $568.67

Opened: October 8, 2020

Also an IRA trade. I’m a sucker for a high-yield REIT. This one has been beaten down by COVD-19, down 55% YTD, and for good reason. Tanger operates high end shopping malls! So this is speculative and, if I end up with shares, hoping that dividend gets going again soon. Also a decent premium for such a cheap stock (because volatility!).

These next four trades are part of my mortgage pay down strategy. You can read my introductory post here. I will have more updates regarding my specific strategy in the future, but essentially it is using extra cash flow, thanks to a refinance, on building a small portfolio concentrating on cash-secured puts and covered calls, and then paying down the mortgage with the premiums generated.

Mortgage pay down strategy. But this one is a little different because it is deep in the money, below my purchase price of $2.34. FCEL is from the dot-com bubble (checkout the historical chart — an all-time high of $7,731 back in September of 2000 and an all-time low of $0.13 last year!), so this one can go all over the place. It’s a small position, so worth the risk I think ($7 in 8 days on a $234 investment is 124% annualized return!).

RKT Put Credit Spread (November 20, 2020 $19/18 @ +$.26)

Max Profit: $26

Collateral: $100

Max Loss: $74

Opened: October 8, 2020

New mortgages are at all-time highs because of the housing and refinance markets, and Rocket is one of the biggest players these days. I feel good about this one holding above the $19 mark.

This year my wife and I took advantage of the record-low interest rates to refinance our personal residence, as seemingly every other household in America has done. We purchased our home just one year ago with what we thought at the time was a solid interest rate of 3.75%. This month, we were able to refinance down to 3.125%, saving us about $200 per month. With property tax and insurance adjustments, our actual monthly Principal/Interest/Taxes/Insurance (PITI) payment reduced by exactly $164.21. Another bonus is that we were able to skip one month of payments since we closed on the new loan in September and October’s payment is not due until November 1 (mortgage is paid “in arrears”). I’ve put my mind to work lately to think about what to do with this extra savings. The number one goal is to not increase our monthly spending by that amount. We are used to making a monthly payment of $3,151.22, so I want to carry on like we are still making that same payment.

The question is what to do with the extra $164.21 to build wealth. There are two simple options that immediately come to mind.

Benchmark #1: Savings Account

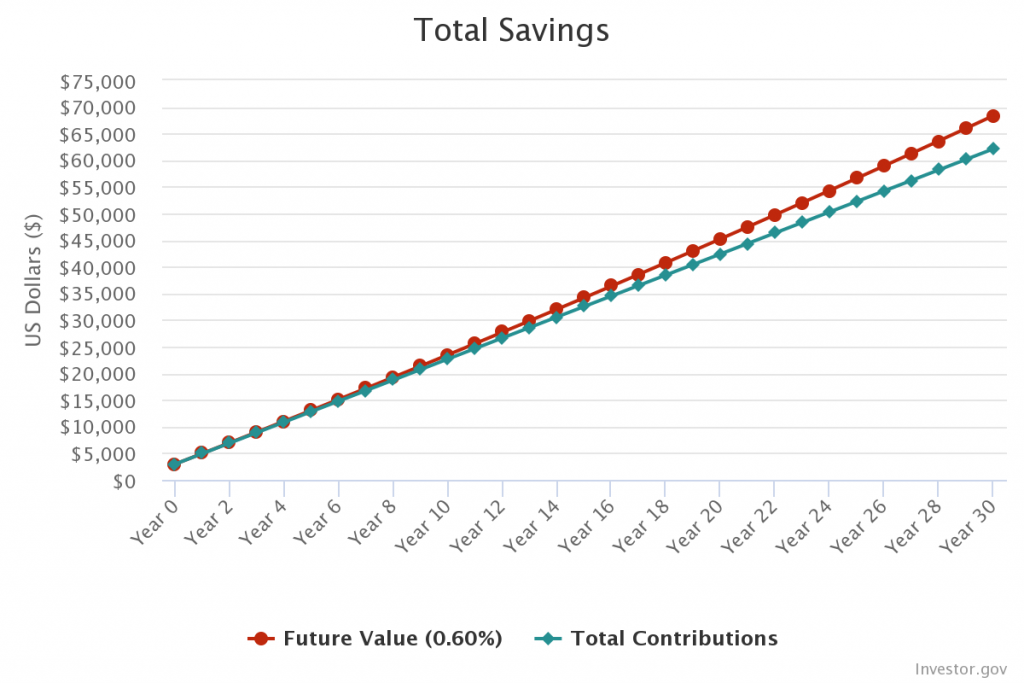

First is to put our first month of no payment (call it $3,000) plus $164.21 each month into a high yield savings account or money market. Our money market is currently earning 0.6% APY (I will use “savings account” and “money market” interchangeably throughout the rest of the post). Assuming that interest rate remains the same over the next 30 years (it won’t), that initial $3,000 plus $164.21 monthly contribution would turn into $68,343.93 (compounded monthly). Compounding interest is a hell of a drug! The biggest advantage of this idea is that it is extremely liquid and the principal is guaranteed by FDIC. When the right investment comes along (e.g. real estate rental property!), I will have this amount at my disposal!

One thing to note is that we already save some of our paychecks in this savings account, which currently sits at around ~6 months of our monthly spending after doing some fairly expensive home renovation projects in the past 12 months (new windows and floors… remind me, is your personal residence an asset or liability?). Whether or not we use this strategy, ultimately I would like to see that savings amount closer to 1 year of expenses. We also have no other debt (student loans, car payments, credit cards). If we did, the $3,000 + $164.21 would immediately go towards paying down that debt first and foremost!

Growth of $3,000 with a $164.21 monthly contribution compounding at 0.6% APY

Benchmark #2: Extra Principal

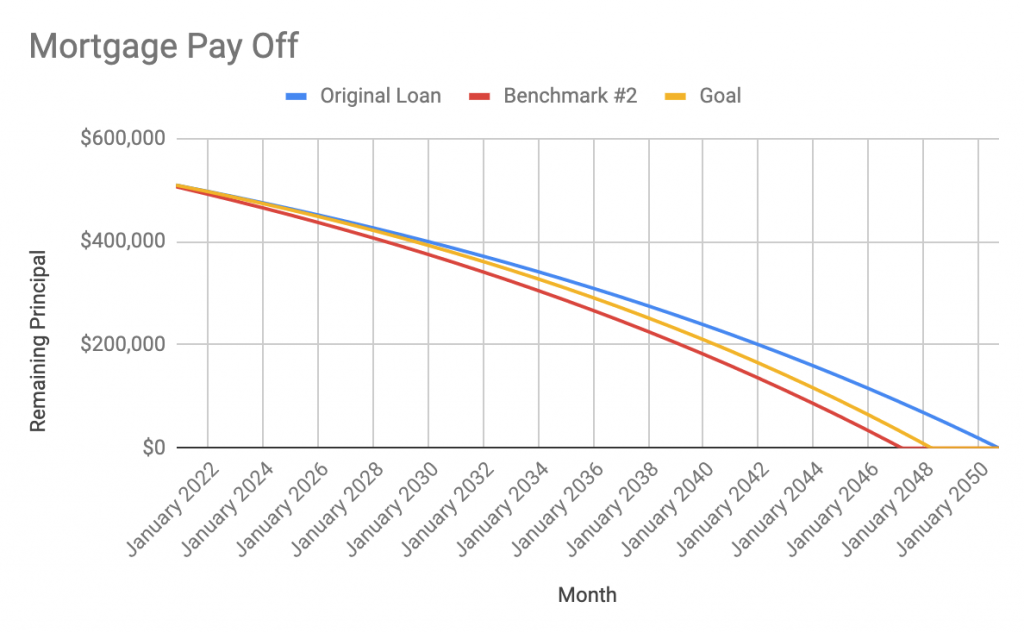

The other simple option is to make an extra principal payment on the loan of $3,000 initially, and then $164.21 each month after that. This would reduce our loan term by more than three and a half years (42 months) and save $37,490 in interest due the extra $54,890 principal payments made. If we then put the $164.21 in the savings account at 0.6% for the remaining 39 months, the sum would be $6,967.99. Adding the extra principal made, interest saved, and the final savings account sum, this strategy comes out to be worth $99,347.99, beating the all-savings option by 45%! The obvious downside here is we don’t have (easy) access to that extra $54,890 we put into equity. We could get a home equity line of credit (HELOC) to access that equity, but if my property value goes down, it’s possible I won’t be able to access any of that equity due to loan-to-value limits (we are currently sitting at about 70% LTV, for the record).

While I love the idea of reducing our $510,400 loan as it will have an immediate and guaranteed impact on our wealth (wealth = assets – liabilities), I think there is a better option, no pun intended.

If I accept a little bit more risk and work it a little bit more, I think I can get the best of both worlds (liquidity and debt paydown) with options trading. But before I go into option trading, let’s draw one more line in the sand for comparison.

Benchmark #3: Invest in S&P 500

Let’s say I put the initial $3,000 and then $164.21 into the S&P 500 and earn the often reported 8% annual yield? That number comes out to an impressive $277,539.11 after 30 years! There are obviously going to be some large market fluctuations in 30 years, but let’s use that as the ultimate benchmark. For the record, as I write this on October 9, 2020, SPY is trading at $346.21. As I go forward with tracking my progress here, I will benchmark against all three of the previous strategies, comparing returns, debt paydown, and principal.

My Strategy

What I plan to do is actually a bit of a hybrid of the three benchmarks. All the specifics of how I’m investing using options will come in future, ongoing posts, but here is the overall strategy/results I’m hoping to achieve.

On the 1st of each month, we will make a $3,151.22 payment from our checking account to the previously mentioned money market account. Prior to refinancing, this was the exact payment we were making for our PITI. From the money market account, we will transfer $100 of that to our brokerage account in which we will be investing. That account’s starting balance is at $3,000*. We will then pay $2,987.01 on the 1oth of the month to our loan servicer. Why the 10th? Because mortgage is due on the 1st of each month, but not late until the 15th. Money market accounts compound interest daily, so we are getting an extra 10 days of compounding interest. Our money market account will now have $64.21 at the end of the month.

*The account is actually already existing with a balance higher than $3,000, but I have earmarked that $3,000, plus additional payments going forward, for this specific strategy. I plan to keep very detailed records so I can really see what my returns are.

Back to the investing account, a percentage of that portfolio’s investments will then go toward paying down the mortgage, with the remaining balance being used for capital appreciation and income taxes at the end of the year. My goal for the investing account is an aggressive 1% return on the principal each month. Of that 1% return, 68.7% will go toward extra principle on the mortgage. Why 68.7%? Because our marginal federal tax rate is 22% and California state is 9.3% (31.3% total). At the end of the year, that 31.3% should more than cover extra tax liability from this income stream.

So for the first month, my investment account principal is at $3,000 and my goal is to generate $30 (1%). $20.61 goes to mortgage principal (68.7%) and $9.39 (31.3%) is set aside for taxes. On month two, my principal is now $3,100 and my goal is to generate $31, with $21.30 going to mortgage principal and $9.70 going toward taxes. And so on…

Now let’s see where my goal for this strategy compares with the other three. My mortgage will be paid down only 29 months early, with an extra principal of $44,133 made, saving $19,851 in interest. My principal in the investing account will be $39,168.40. Meanwhile, over in the savings account, the $64.21 monthly savings will have accumulated to $25,319.74. The sum total of this strategy is now $128,472. This is 88% better than all savings (Benchmark #1), 29% better than all principal payments (Benchmark #2) and 54% worse than just investing in the S&P500 ETF (Benchmark #3).

Comparing Original Loan with Benchmark #2 and Goal Strategy

When comparing my strategy to the other benchmarks, it’s important to consider the potential returns, risks to the principal, liquidity and how passive the strategy is. Below is a table ranking each strategy, with 1 being the “best”.

Strategy

Potential Return

Principal Risk

Liquidity

Passive

Benchmark #1

4

1

1

1

Benchmark #2

3

2

4

1

Benchmark #3

1

4

2

3

Hybrid

2

3

3

4

Clearly, my hybrid approach is a mixed bag. It is by far the least passive approach, but because of that, there is a potential for increased returns that the others don’t have, and that’s what excites me! One thing to also note is that taxes were not considered in the other three benchmarks. Interest from savings accounts are subject to ordinary income tax, mortgage interest is tax deductible, and stocks are taxed as income or longterm capital gain depending on holding period. For that reason, my hybrid strategy, in which I am accounting for taxes, is a much more realistic return.

Finally, what are the odds that I stay in this home for the next 30 years? What about keeping up with this strategy? Or writing this blog! Of course none of it will likely be going in 30 years, but I will keep this up to date and going for as long as I can/am able/am willing to!

This week kicked off my first full week diving into the world of options trading. I’ve been interested in stock market investing since I graduated high school in 2006. At one point in college I thought I could be a day trader, but then had a short series of losses that made me reconsider the viability of that. If this goes well, perhaps I will go into further detail on how I ended up on options trading. But for now, I’m looking to post weekly trading reviews (and perhaps a monthly review as well) to hold myself accountable and to have a history to look back on. Let’s get started…

Closing Previous Weeks’ Trades (Positions closed that were opened previous to this week)

GPRO Naked Put (October 16, 2020 $4.50 @ +$.55 Credit)

Contracts: 1

Max Profit: $55

Collateral: $450

Max Loss: $395

Opened: September 24, 2020

Closed: September 29, 2020

P/L: $26.66 (After commissions)

Return on Capital: 5.9% (360% Annualized)

This trade was in my regular brokerage account that hasn’t been approved for Level 3 Option trading yet. So silly that they will let me trade naked puts (so long as they are “cash secured”), but not risk-defined spreads. Anyway, sold this put just above the money, giving me a solid premium. My goal on this stock (and this account in general, at the moment), is to sell aggressively priced puts (at the money or even just above), knowing that I will likely be assigned. Then, I will sell calls if/when I am long the stock with 100 positions. I closed this one based on a GTC limit order at roughly 50% max profit. Actively looking to get into another one of these.

This was my first calendar spread. I found this using the Option Alpha scanner ($47 for a lifetime access). Since I’m just getting my feet wet here, I wanted to take the early profit. Looking to get into another one of these in the future.

AFL Naked Put (October 16, 2020 $35 @ +$.70)

Contracts: 1

Max Profit: $69.33

Collateral: $3500

Max Loss: $3430

Opened: September 17, 2020

Closed: October 2, 2020

P/L: $38.67 (After commissions)

Return on Capital: 1.1% (25.2% Annualized)

I’m bullish on most insurance companies, generally speaking, and am looking to add some to me and my wife’s retirement portfolio. We have some cash in there thanks to a rollover from a pension that my wife had from a previous employer she worked a couple years with. I’m going to put that cash to work with naked puts. The plan is to sell puts on companies I want to have in our portfolio (ideally ones with a solid dividend — Aflac currently yields 3.1% and they have grown their dividend for 38 consecutive years! A true dividend aristocrat.). If the stock expires out of the money, then I keep the premium and purchase one or two shares of the stock. If it expires in the money, I will sell some covered calls to guarantee a return on that capital. When doing this on strong companies (like big insurance companies!), this really feels like a win-win. Ultimately I closed the contract early since I was able to guarantee the premium necessary to purchase one share. Rinse and repeat!

AAL Put Credit Spread (October 16, 2020 $11.50/10.50 @ +$.31)

I jumped into AAL after COVID-19 hit and it started spiraling downward. I was just a simple stock investor then and hadn’t wised up to options trading yet. I am currently long 68 shares at an average price of $14.69. This stock has been trading in a range between about $11 to $14 and I think I have a good feeling for its price movement. With some good news eventually, I expect this to actually pop and I will get out of my long position. I decided to close out of this position on Friday since it shot up from $12.26 to $13.33 on news that they would be furloughing 32,000 workers. Hardly seems like good news to me… so decided to take the opportunity to snag a profit.

Weekly Roundtrip Trades (Positions opened and closed within the week)

I have made a number of trades in TSLA because I like the option premiums there (implied volatility is high). NKLA sneaks into some of the headlines since it’s a recent IPO competitor. I took a look at the premiums on offer, and I liked what I saw. The stock jumped up the next morning, and since this is a pretty speculative play on a stock with a 52-week range of $10.20-93.99, I figured I’d take my quick profit. Will consider trading this one again.

NKE Put Credit Spread (October 16, 2020 $125/124 @ $.40 Credit)

This is a trade I immediately regretted once I hit send. I got into it because I have a Call Credit Spread at $125/126 which was a pure, bearish speculative trade before earnings last week. That position is currently at a loss with the stocking sitting around $126. My original thinking here was to reduce my loss on the initial Call Credit Spread, but then I immediately realized that we have three weeks for the stock to come back in my profitable range. Happy to get out of this one for a small $5 profit. I think this might be a viable strategy, but only as we get closer to expiration.

You are going to see plenty of SPY trades in my trading journal. A critical component to success in high probability options trading is that you need to be making a high volume of trades, ideally in very liquid stocks. With three expiration dates per week (Mon/Wed/Fri), SPY appears to be the perfect candidate. I am working out my strategy still, but on this trade specifically I wanted to take a bearish position when the market jumped up on Monday morning this week. In hindsight, I think I should be looking beyond a one-week contract as there is more time “to be right”, but this one worked out. I did, however, get tested with the market climbing up just past my break even point in the middle of the week. Luckily I stuck it out (though I added a put position that I’m probably going to regret on expiration next week), and thanks to President Trump’s timely COVID-19 diagnosis, the market opened down on Friday morning. I took the profit on a silver platter. Thanks Donald!

As I said in my AAL trade above, I feel comfortable about the range of AAL. Implied volatility is pretty high for AAL right now and there are plenty of trades that look good from a risk/reward/probability standpoint. Since I am long this stock, this gives my portfolio some bearish upside, as well. Looking for about 50% of max profit.

SQQQ Put Credit Spread (October 16, 2020 $22.50/22 @ +$.20)

Contracts: 1

Max Profit: $20

Collateral: $50

Max Loss: $30

Opened: September 28, 2020

SQQQ is a 3x leveraged ETF of the Nasdaq. This is effectively a bearish position on the market. I personally think It will make a move down, which will make SQQQ go up and I should be able to close this one for a profit if and when we see a jump up in price of the stock. Risk-reward was really good on this trade, as well, thanks to very high implied volatility and only $.50 spread.

Basically the same justification as above, but with a longer timeframe.

ANF Put Credit Spread (November 20, 2020 $13/12 @ +$.35)

Contracts: 1

Max Profit: $35

Collateral: $100

Max Loss: $65

Opened: September 29, 2020

This might sound crazy, but my wife says she has seen lots of “influencers” on social media sporting Abercrombie lately. She thinks it’s going to be a “cool” brand again. I took a look at the premiums available, and they make sense from a risk-reward-probability perspective, so I pulled the trigger. That’s one of the things I love about options trading is that for a small amount of capital, you can make speculative trades that are still high probability of success regardless of whether the stock moves much at all AND have defined risk.

In the past few weeks I’ve really dove head-first into options trading, and I have Option Alpha to thank (blame?). On their most recent podcast, this trade in XLV was featured on their “Closing Bell” segment, though they took a much bigger spread at 108/113, I believe. I checked the chart and options available, and the trade still made sense to me.

The market moved up on Wednesday, so I’m challenging it with this position. Similar to the closing trades for SPY that I mentioned above. This one didn’t close on Friday like the other two due to the Trump COVID-19 induced pullback..

VIX

Put Credit Spread (November 18, 2020 $27/26 @ +$.41)

Max Profit: $41

Collateral: $100

Max Loss: $59

Opened: September 30, 2020

This is a speculative trade. The probability was a lot lower than the other trades I’ve been making (56% vs ~70%), but the payoff is decent and I think as we continue to move toward the election that we will see an increase in volatility, pushing the VIX higher. I actually sold this position in the money (trading at ~$25.50 when I placed the trade), hence the larger premium and lower chance of profit.

SPY Put Credit Spread (October 5, 2020 $335/334 @ +$.28)

Max Profit: $28

Collateral: $100

Max Loss: $78

Opened: October 1, 2020

This is my second attempt at reducing a potential loss by selling the opposite trade, effectively making an iron condor. Option Alpha recommends this rather than cutting losses by selling the initial, losing trade (in this case the $341/342 Calls that ended up being profitable thanks again to the dip from the president’s COVID-19 results).

Same XLV trade as listed above, but decided to add essentially the same position in another portfolio.

GPRO Naked Put (October 9, 2020 $5 @ +$.50)

Max Profit: $50

Collateral: $500

Max Loss: $450

Opened: October 1, 2020

After successfully closing last week’s short put on GPRO, decided to do another one. If I get assigned, I will sell calls at probably $5. If I don’t, I will probably buy a few shares of GPRO essentially “for free.”

QQQ Put Credit Spread (November 6, 2020 $264/263 @ $.32)

Max Profit: $32

Collateral: $100

Max Loss: $68

Opened: October 2, 2020

Tech was down quite a bit on Friday, so taking a similar strategy that I have going right now in SPY now in QQQ.

PMT Naked Put (October 16, 2020 $15 @ $.20)

Max Profit: $20

Collateral: $1,500

Max Loss: $1,380

Opened: October 2, 2020

PennyMac Mortgage Investment Trust is a stock I came across recently that is obviously invested in real estate. It caught my eye because it is local to me and its dividend currently yields over 9%. I’m planning to continually sell some out of the money puts on PMT and then invest premiums into buying the stock.

TSLA Put Credit Spread (October 16, 2020 $388/387 @ $.32)

Max Profit: $32

Collateral: $100

Max Loss: $68

Opened: October 2, 2020

TSLA had a bit of a sell-off. I think this stock is way overpriced, but was able to get a ~70% probability trade at nearly $40 below current market price.